Is it still possible to claim a tax deduction for any financial loss suffered due to theft and other unforeseen events even if the property was insured? Generally, the answer to this is “Yes”, but only for the unreimbursed portion and only if it meets IRS’ criteria. Want to know more? Here’s how.

The Basics

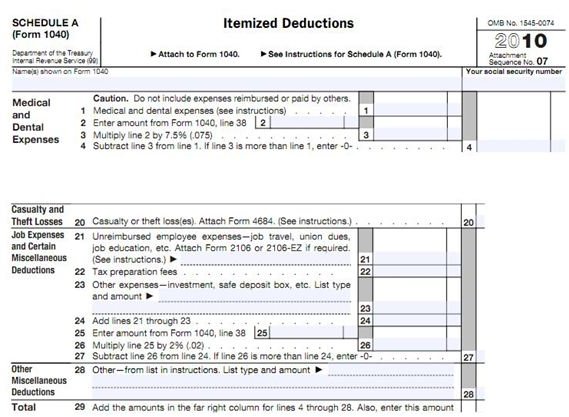

The Internal Revenue Service (IRS) refers to financial loss that took form as a result of damages and destruction of properties as “casualty loss”. Tax deductions to reduce one’s tax liability are allowed if a taxpayer meets all requirements and makes a claim by using the “itemized deduction” on Schedule A of IRS Form 1040.

In addition, there are two premises to consider in determining the personal casualty loss deduction limitations. The first is the stipulated $100 limit, which denotes that the first $100 value of the loss is not eligible as tax deductions.

The second is the 10 percent rule, which is based on the taxpayer’s adjusted gross income or AGI as it determines the taxpayer’s income threshold to sustain or absorb expenses or losses. If the 10 percent rule is greater than the loss, then the amount being considered as tax deduction is not eligible. On the other hand, if the amount of loss is greater than 10 percent of the AGI, the established amount of loss less the 10 percent equivalent is the allowable amount of casualty loss deduction.

Providing Examples and Explanations of Calculations

Claiming Tax Deductions for Loss of Personal Property:

Ordinarily, a simple financial loss is deducted in the tax year of the same year when the unexpected event took place. All one has to do is to reduce the amount of loss by the amount collected as insurance reimbursement (if there is any) and the personal deduction limitation. Do those in order to arrive at one’s personal casualty loss deductible. To illustrate:

A taxpayer suffered a total loss of $3,000 when his parked car was rammed by a wayward vehicle. The car’s insurance policy has a $2,000 deductible, which means the insurance company had reimbursed only the losses that exceeded $2,000. That being the case, $2,000 of the $3,000 damage was not reimbursed by the insurance company. If the taxpayer’s AGI for the year is $18, 000, the amount of tax deduction will therefore be computed as follows:

- Amount of Financial Loss- $3,000

- Less: Reimbursed Amount- $1,000

- Net Loss Sustained - $2,000

- Personal Loss Deductible – ($100)

- Adjusted Deductible Loss - $1,900

- 10% of AGI Rule – ($1,800)

- Amount of Casualty Loss Deduction- $100

However, if the taxpayer’s AGI for the year is $20,000, the taxpayer’s 10% AGI will be higher at $2,000. No amount of tax deductible can be claimed as deductions for losses on personal property damages. The rationale for this is that the threshold limit of the taxpayer’s AGI, against losses and expenses, is still enough to buffer the $1,900 personal loss.

This basic computation is likewise applicable in determining the tax deductible amount for losses due to theft, robbery, embezzlement, kidnap-for-ransom, blackmail, extortion and larceny. However, complexities arise as other types of property losses depend on varying factors as bases for calculating the allowable tax deduction.

Claiming Tax Deductions for Losses on Damaged Property

In calculating the amount of tax deductible for losses on damaged property, which was caused by unforeseen events like hurricanes, tornadoes, earthquakes, fires or similar catastrophes, the values of the additions erected on the entire property, i.e. building, fence, trees, decks, and so forth are treated as a single loss.

There are two values considered for calculating the amount of deductible loss and the smaller of these two values shall be used:

(1) The Fair Market Value (FMV) after the catastrophe

Basically, the context of fair market value means it is the price which a buyer of the property would be willing to pay while knowing the conditions surrounding the property. Neither the buyer nor the seller is looking for a property to sell or buy immediately after the untoward event.

(2) The adjusted basis of the property, which is the original cost plus the add-ons or improvements, minus all the value of depreciations and / or depletions of the property.

Example:

A taxpayer owned a house and lot, which he had bought a few years ago at a price value of $115,000, and for which he spent an additional $65,000 for some repairs on the improvement and landscaping .

Unfortunately, a hurricane destroyed the improvements, but the insurance company reimbursed the taxpayer the amount of $100,000.

Due to the increasing number of hurricanes that had hit the region, the FMV of similar residential properties had dropped to $175,000 from a FMV of $300,000 before the hurricane had taken place. The taxpayer’s AGI for the year is $60,000.

Calculating the amount of loss from property damage is as follows:

- Adjusted basis of the property ($115,000 + $65,000) - $180,000

- FMV before the hurricane - $300,000

- FMV after the hurricane - $175,000

- Loss Due to Decline in FMV - $125,000

Before proceeding to the next steps, it should be noted that the value to be used as a basis for calculating the amount of tax deduction is the loss due to the decline in FMV, which is $125,000.The latter has a smaller value than the adjusted basis of the property worth $180,000.

Determining the amount of claim for tax deduction:

- Loss due to decline in FMV - $125,000

- Amount of insurance – ($100,000)

- Loss after insurance - $25,000

- $100 personal deduction limit – ($100)

- Loss after the $100 rule - $24,900

- 10% of $60,000 AGI – ($6,000)

- Casualty Loss Deduction - $18,900

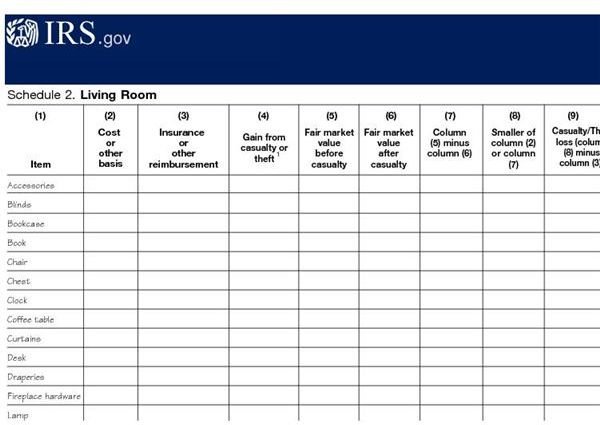

Claiming Tax Deductions for Losses on Damaged Property with Furnishings

Let us suppose further that the property lost in the previous example had valuable furnishings. The taxpayer may take into consideration the FMV for each type of valuable in order to determine the total amount of loss suffered.

Prepare a worksheet listing all the furnishings that were damaged, and then determine the value of the loss by comparing the smaller amount between the adjusted basis and the loss from the FMV before and after the unforeseen event. Aggregate the losses sustained from all the furnishings that were damaged or destroyed. For this purpose, we will use as an example the amount of $15,500 for said losses, while the amount of insurance reimbursement received was worth $10,000.

Using the calculations for the previous example, the computation for the total casualty loss will be modified as follows:

-

Loss due to decline in FMV - $125,000

-

Amount of insurance on real property – ($100,000)

-

Loss on real property after insurance - $25,000

-

Loss on furnishings - $15,500

-

Amount of insurance on furnishings – ($10,000)

-

Loss on furnishings after insurance - $5,500

-

Total Losses on real property and furnishings – $30,500

-

Less the $100 personal deduction limit – ($100)

-

Loss after the $100-rule - $30,400

-

Subtract 10% of $60,000 AGI- ($6,000)

-

Total amount of casualty loss deduction - $24,400

Other Salient Points to Consider

(a) The above computation shows that the personal deductions limit of $100 and 10 percent rules are being applied on a per event basis and not per item of property damaged or destroyed. For purposes of reporting these losses and presenting the manner on how the amount of tax deductible loss was arrived, the taxpayer will use Form 4684. A more comprehensive set of instructions is being used by taxpayers as reference for instructions, which is the “IRS publication for Form 4684- Casualties and Theft”. (See the link in the Reference section below).

(b) If two or more persons share ownership of a damaged property and they are not married or do not file a joint income tax return , each individual applies the $100 and the 10 percent rule individually when calculating the tax deductibles for their individual share of losses. This is regardless of if the event referred to is one and the same.

(c) For losses suffered as a result of calamitous events, which were subsequently declared by the government as federal disasters, the taxpayers are being given special privileges as a means to help them immediately recover from their losses. They can choose to treat the claim for the deduction as if it was applicable to the year previous to the actual year when the calamity actually happened. The claim can be made by declaring it as a previous year’s adjustment of the current return being filed.

To illustrate by way of example: Suppose the loss being claimed was a result of a 2010 hurricane declared as a federal disaster. This means that the taxpayer can opt to treat his 2010 losses as if they were sustained in 2009. This is done by reporting the casualty loss deduction as a tax adjustment for 2009.

(d) As a rule, tax deductions for casualty damages during the year can only be made if a timely claim for insurance reimbursement has been made or if there is no insurance reimbursement to be deducted against the loss suffered.

In all types of claims for theft and casualty loss deductions, the most critical requirement is the show of proof that there was actual loss suffered and that the amount being claimed as the loss can be substantiated by supporting documents.

Reference Materials and Image Credit Section:

References:

- IRS Publication 547 - Main Content Casualty and Theft Loss – https://www.irs.gov/publications/p547/ar02.html#en_US_2010_publink1000225406

- 2010 Instructions for Form 4684 Casualties and Thefts – https://www.irs.gov/pub/irs-pdf/i4684.pd

Image Credits:

- Image of Form 1040 Schedule A / IRS.gov .

- Image of IRS Worksheet for Calculating Loss on Furnishings– IRS.gov

- Image: Aerial view of houses destroyed by 2011 tornado; Western MA by Massachusetts Department of Environmental Protection under CC BY 2.0