Investment income is typically comprised of dividends plus annual capital gains. There are other forms of investment income; however, these are the most common. Investors who have failed to file a W9 form with an investment firm may be subject to backup withholding reducing the amounts paid out.

What is Backup Withholding?

Backup withholding is tax an investment firm is required to withhold from distributions on certain types of investment income in the event an investor has failed to provide a W9 form to the company. Backup withholding is a mandatory reduction of income received capital gains distributions, interest on certain investments and dividends that are earned on stocks or mutual funds. The funds are withheld from these distributions and they are sent directly to the Internal Revenue Service and credited to the account of the taxpayer. This means that when the taxpayer files their taxes at the end of the year, their tax burden on investment income will be reduced by the amount that was withheld during the year.

What is the tax withholding on investment income?

The amount that is required to be withheld was established by the Internal Revenue Service in during 2002. At that time, the rate of backup withholding was set at 28 percent. The rate went into effect on all earnings after December 31, 2002. This amount will be charged on income through December 31, 2012 at which time it will be reviewed again.

Can I avoid backup withholding?

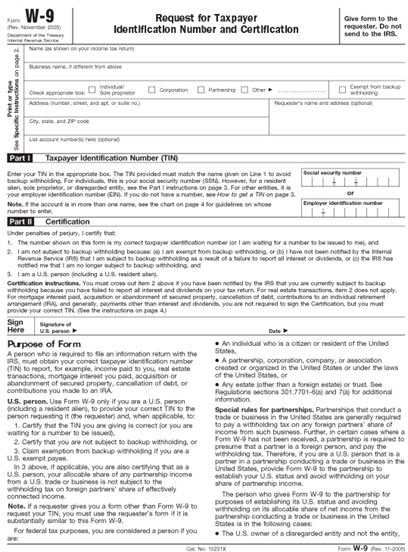

Backup withholding is required when the taxpayer has not certified their social security information with the investment company. This can be remedied by filing a form W9 and by stating under penalty of perjury that the shareholder is not subject to backup withholding. The form is two-fold; it verifies the social security number belongs to the shareholder as well as verifying the shareholder is not subject to mandatory withholding.

Investments Excluded From Withholding

Various investment accounts that are set aside for retirement, education and long-term savings such as bank certificates of deposit, stocks, bonds and mutual funds or other investments like real estate or life insurance are typical investments that taxpayers consider when establishing an investment portfolio.

Most stocks, bonds and mutual funds (as well as bank certificates of deposit) may be subject to backup withholding taxes, not all investment income payees are required to withhold taxes. This includes cases where a shareholder has not filed a W9 form. Some of these include:

Income from long-term care benefits - Investors who have earned interest or dividends on long-term care plans are not subject to having part of their benefits withheld for tax purposes. While this income may still need to be claimed, the investor will receive this amount in full.

Income on qualified retirement plans - Company sponsored benefit plans such as Employee Stock Ownership Plans (ESOPs) are not subject to withholding. Earnings will need to be claimed on the shareholders tax forms but they are not subject to having taxes withheld at the time of distribution.

Income tax refunds - Income tax refunds on both the state and federal level are free from backup withholding requirements. These funds must be paid to the taxpayer even if their social security number is not verified using a Form W9. Taxpayers may face other levies on their refunds but this is not one that they will have to be concerned about.

Other income that is not subject to backup withholding includes (but is not limited to) unemployment compensation, real estate transactions and canceled debts. Investors who believe they may be subject to backup withholding taxes should contact the Internal Revenue Service for additional information. Losing 28 percent of investment income on each distribution can be very costly for those with a significant investment portfolio. In most cases, filing a W9 form will help an investor keep more of their earnings.

Resources

Sources

- Investopedia Backup withholding definition

- Internal Revenue Service Backup Withholding “B” Processes

Image Credits

- Form W9 via wikimediacommons.org/Public Domain from IRS

- Savings bank via wikimediacommon.sorg/Public Domain from GeorgHH