Learn when and how to get a car tax deduction for charity. Find answers to the questions: where can I donate my car for a tax deduction and what documentation do I need to support my deduction on my taxes? By knowing what you’re getting into, you can save yourself trouble down the line.

Each year, millions of people make charitable donations, some in the hope of lowering their tax liability and others for the internal satisfaction received from giving. Making a donation can be beneficial financially if you do a little planning ahead and know the documentation necessary. With most non-vehicle donations, having a receipt with the date, address, and description of the donation is enough to include the value of the donation on your Schedule A tax form as a deduction, however there are instances when more details are required. Specifically, when the value of your vehicle is greater than $250, you will need more documentation in order to claim the deduction on your taxes. This article will hopefully help you navigate the documentation necessary to claim your donations on your taxes next year.

When Can I Take a Donation?

The first, and most important, step toward claiming a vehicle donation on your taxes, is to know when you are able to claim a donation. A vast majority of people are not able to claim donations, vehicle or otherwise, because it does not help to lower their tax liabilities and in fact, sometimes, could hurt their liabilities.

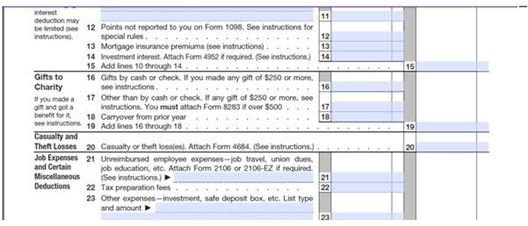

Charitable donations, including donations of items, cars, household goods, and time, are claimed on the Schedule A . The Schedule A is not always filed with every return, a vast majority of filers don’t use the Schedule A. If you have itemized your deductions in the past on your taxes, then you use the Schedule A to show those itemized deductions. Check the instructions for the Schedule A on the IRS website, www.irs.gov , to determine whether or not you will benefit from itemizing your deductions.

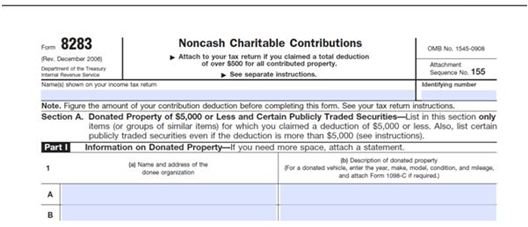

In general, if the items donated are valued at less than $250, you must provide the date of the contribution, amount of the contribution, and the name of the organization receiving the contribution. So if you donate a vehicle with a value at less than $250, it is treated as any other donation and the item is listed along with the qualifying organization receiving the donation and the approximate value at the time of donation. If the value is greater than $250 then you must also have documentation of the vehicle donated. If the value of the vehicle is greater than $500, you will

need to fill out Form 8283 as well as keep the documentation already listed.

If itemizing your deductions is not beneficial, then you will not be able to claim the donated vehicle on your taxes for this year. There are however rules on carryover donations which may allow you to claim the donation in a subsequent year. Additionally, if you receive any goods or services in exchange for the donation, you must subtract the value of those goods and services from the amount you donate.

Donating a Motor Vehicle, Boat, or Plane

The process to claim a donation of a motor vehicle, boat, or plane is different than claiming a donation of time, clothes, or money. In 2004, the rules changed when determining the value of the vehicle. First, determine how much the vehicle is worth. If the vehicle is worth more than $500 you have two options for claiming the deduction based on what the organization does with the vehicle. If the organization sells the vehicle, you may claim the gross proceeds of the sale of the item. You should receive a written notice of sale within 30 days of the sale. This notice will state the value of the gross proceeds you’re allowed to claim on your Schedule A. You will need to provide that notice of sale to the IRS with your tax return.

If the charitable organization instead uses the item or improves it significantly, you are allowed to deduct the fair market value of the item. The organization would need to submit verification that the item is intended for use and/or improvement. This should be received within 30 days of the donation as well. Again, this documentation would need to be submitted with your tax return.

If the value of your item is less than $500, then you can deduct the fair market value up to $500. Anything over the $500 threshold is subject to the guidelines listed above.

Qualifying Organizations

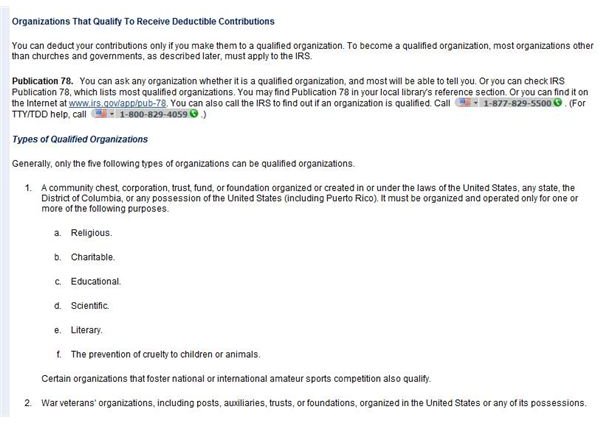

Another important question to ask is where can I donate my car for a tax deduction? It is important to determine who is qualified to receive the donation. This is as important as valuing the item because the IRS will only allow deductions made to qualifying organizations. If you make a donation to a non-qualifying organization, you will not be allowed to take the deduction. The IRS has a publication specifically written to layout the guidelines for charitable contributions. In general, if the organization is in one of the following categories as listed on the IRS website, then your donation can be tax deductible.

1. Religions

2. Educational

3. Charitable

4. Scientific

5. Literary

6. The prevention of cruelty to children or animals

These six categories are not exhaustive. Additional qualifying organizations include: war veterans’ organizations, domestic fraternal societies operating under the lodge system, certain nonprofit cemetery corporations, the United States or any state. As there are a large number of categories that qualify, it is best to determine whether or not the organization qualifes under the IRS guidelines prior to making a charitable donation. If you are unsure, after reviewing the IRS guidelines, you can call the IRS directly and find out if the organization would qualify for a charitable tax deduction.

Conclusion

In conclusion, it is important to make sure you assign the appropriate value to your donated items and document the items you wish to donate. If you donate a motor vehicle, boat, or plane with a value greater than $500, you will need documentation from the organization receiving the donation in order to claim the value on your tax return Schedule A form. If you instead donate items that are valued at less than $500, you can claim a fair market value on your items.

Additionally, when claiming a deduction you must subtract the value of any goods or services you received in exchange for the donation.

If you do not have enough itemized deductions to use a Schedule A, then your donation can not be claimed during that tax year unless you wish to risk a higher tax liability. If you can not claim your donations as a deduction on the Schedule A for the current tax year, you may be able to claim a carryover deduction in a subsequent year when filing a Schedule A is beneficial to your tax liability.

References

Image Credits

Image 1 (“Form 8283”): https://www.irs.gov/pub/irs-pdf/f8283.pdf

Image 2 (“Schedule A Donations”): https://www.irs.gov/pub/irs-pdf/f1040sa.pdf

Image 3 (“IRS Qualified Organizations”): https://www.irs.gov/publications/p526/ar02.html