While payroll deductions for Medicaid are the same regardless of how much you make, annual caps on Social Security earnings impact thousands of employees as well as those who are self employed each year. During 2011, Social Security withholding rates have an impact on all workers.

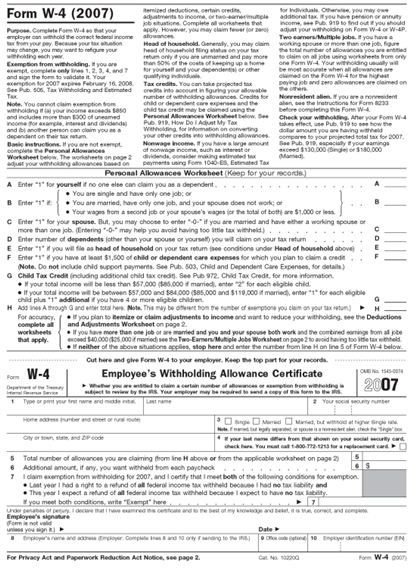

W4 and Tax Withholding

Those beginning a new job are asked to fill out a W4 form along with numerous other documents that relate to their employment. Form W4s are designed to obtain information from employees about the amount of funds that are to be deducted from their paychecks for State Tax Withholding, Federal Tax Withholding and supplemental amounts (if any) to be withheld. Employers are advised by the Internal Revenue Service to ask employees to verify their withholding amounts on a regular basis. If the employee received a large refund, or was required to pay taxes on either state or federal level, the withholding allowances can be adjusted upwards or downwards.

The two standard deductions from payroll taxes are Social Security withholding and Medicare withholding. These amounts are not impacted by the number of deductions that an employee claims on their form W4, instead, they are a percentage of their payroll check. Some forms of income such as educational assistance income, life insurance benefits and accident and health benefits are not subject to Social Security or Medicare withholding although they are subject to state and federal tax withholding.

Caps on Earnings

Federal and state taxes and Medicare withholding are taken from all qualified earnings from each employee. Social security on the other hand faces an earnings cap. Employees who earn more than $106,800 will have their percentage of their Social Security taxes withheld from their paychecks.

Social Security and Medicare withholding is divided between the employer and the employee. Medicare does not have an annual cap on earnings, however, Social Security income does. The percentage that is deducted from the employee also varies; Medicare withholding is 1.45% withheld from the employee and 1.45% that is paid by the employer. Social Security withholding prior to January 1, 2011 was set at 6.2% for employees and the same amount by employers. In order to stimulate the economy and put more money into the pockets of employees the federal government reduced the Social Security withholding rate for 2011 to 4.2% for employees. The employer amount remains at 6.2%. This means a total of 10.4% is being paid into Social Security for the benefit of the employee.

Self Employment and Social Security

Self-employed individuals are not free from paying Medicare and Social Security taxes. Individuals who are employed are not allowed to deduct Social Security or Medicare tax on their taxes, while those who are self-employed are allowed to deduct fifty percent of these taxes. However, they must also pay these from the gross proceeds of their business. Those who are self-employed are required to pay Social Security taxes and Medicare taxes on all amounts that are earned over $400. The same annual earnings cap of $106,800 is applied to those who are self employed. The reduction of 2% in Social Security withholdings also applies to those who are self employed, during 2011 the maximum amount paid will be 13.3% which reflects 10.4% for Social Security and 1.45% for Medicare. Once a person who is self-employed earns $106,800 they will no longer be subject to Social Security tax but must continue paying Medicare tax.

Resources

Sources

Internal Revenue Service

- IRS Publication 15 Circular E Employer’s Tax Guide https://www.irs.gov/pub/irs-pdf/p15.pdf

- Self-Employment Tax (Social Security and Medicare Taxes) https://www.irs.gov/businesses/small/article/0,,id=98846,00.html

Image Credits

- Form W4 Via wikimediacommons.org/Public Domain

- Social Security Card via wikimedia commons/Public Domain

- Tax Deductions via freedigitalphotos.net/Arvind Balaraman