Inflation-proof bonds sounds like an oxymoron, but they do exist in Treasury Inflation Protected Securities (TIPS). Find out about their relation to the consumer Price Index (CPI), what they are, when to invest in TIPS, and when not to.

At the end of a recession it seems that conservative investing becomes the rule of the day for many investors. The most conservative investment for any portfolio would be US Treasury bonds. Treasuries offer a fixed income at low interest rates, but the risk is considered nonexistent, and they aren’t taxed by states and municipalities. The only downside to this is that no matter how safe a conventional bond happens to be, it is always susceptible to the possibility of inflation setting in and eating away at its returns. Adding a measure against this happening is where Treasury Inflation-Protected Securities (TIPS) can come into play for an investment strategy. When to invest in TIPS, and when not to invest is important.

Treasury Inflation Protected Securities (TIPS)

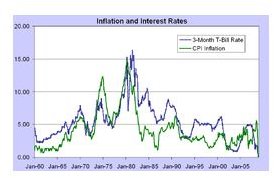

Treasury Inflation Protected Securities (TIPS) were introduced in 1997 and are an effort to provide a US Treasury bond that provides a consistent return at an inflation-adjusted rate. The way that this is done is by making adjustments to the principal for inflation, or deflation as indicated by the Consumer Price Index (CPI), and the interest rate stays fixed. The adjustment is reflected in the increased or decreased, semiannual interest payments; at maturity the investor receives the greater of the adjusted principal or the original principal.

AcquiringTIPS

TIPS are sold at auctions by the US Treasury and they are sold on the secondary markets. Their price is determined at the auction, the current Consumer Price Index (CPI) being the determinant. The US Treasury has its own website for purchasing them called TreasuryDirect, or they can be purchased through banks, brokers, and dealers. They require a minimum purchase of $100 and the maximum that can be acquired is $5 million. Their maturity dates are 5,10, and 30 years.

The months during the year that TIPS are auctioned and the months of reopenings are:

5-year TIPS - April (Reopening: August, December)

10-year TIPS - January (Reopening: March, May, July, September, November)

30-year TIPS - February (Reopening: June, October)

How TIPS are Used

TIPS are used for adding some inflation protection to the fixed income allocation of investment portfolios , or they can be purchased in a more tactical vein, on their own, in anticipation of increased inflation. The addition of TIPS to the fixed income investments of a balanced portfolio can help to lessen the volatility of those investments, just as fixed income securities help to lessen the volatility of the complete portfolio.

Of course, as payments increase with inflation they can also decrease with disinflation, or deflation. This makes nominal bonds (bonds not adjusted for inflation) much more attractive to investors, as their payments stay at a fixed amount during times of economic downturns.

An expected inflation rate can be determined for long terms by comparing a TIPS yield-to-maturity (YTM) with the yield of a similar, nominal US Treasury bond. For example:

A TIPS bond was purchased at an auction at a YTM of 2.5% with a 10 year maturity that is due on January 15, 2014.

A similar US Treasury bond was purchased at a YTM of 4.5% with a 10 year maturity that is due on the same day.

YTM (US Treasury) 4.5% - YTM (TIPS) 2.5% = real rate of return 2%

Subtracting the YTM of the TIPS from that of the US Treasury bond equals a real rate of return of 2% for the US Treasury bond. This is also considered the government’s approximation of the expected inflation rate for these investments.

If an investor is expecting that the rate of inflation will increase to 3%, he would want to invest in TIPS as they will become more valuable in the future against market expectations. The opposite also holds true as the rate of inflation decreases which may cause an investor to sell, or wait for the price to be adjusted downward.

TIPS are unique in that they are the only US backed securities that are inflation-protected and considered risk-free. because of this, they are a valuable addition to any investment portfolio for reducing volatility. They also offer value as a vehicle for speculation on the bond market; but, due to their low return in relation to transaction costs, and, an inability of the government to predict short-term market movements, they should be considered for investing strategies that are looking at more long-term horizons. Knowing when to invest in TIPS is important to earning profitable returns.

Resources

Fred Kaifosh,B.Sc., M.Sc. (Biochemistry), M.B.A., “Why The Consumer Price Index Is Controversial,” 2010. Investopedia. Retrieved November 12, 2010 from the World Wide Web: https://investopedia.com/articles/07/consumerpriceindex.asp#12895906312902&close

Eric Petroff, “Treasury Inflation Protected Securities,” 2010. Investopedia. Retrieved November 12, 2010 from the World Wide Web: https://www.investopedia.com/articles/bonds/07/TIPS.asp

Undisclosed, “Treasury Inflation-Protected Securities (TIPS),” TreasuryDirect. Retrieved November 12, 2010 from the World Wide Web: https://www.treasurydirect.gov/indiv/products/prod _tips_glance.htm

Undisclosed, “Overview of Inflation-Indexed Securities,” 2010. US Department of the Treasury. Retrieved from the World Wide Web: https://www.treas.gov/offices/domestic-finance/key-initiatives/tips.shtml