Fixed income investments can lessen the impact of economic turmoil on a portfolio. What are the types of fixed income investment, and are they worthwhile?

The types of fixed income investments are quite varied and what is considered worthwhile for an investment portfolio depends on the objective of the overall investing strategy. A conservative fixed income portfolio, possibly for a retirement, might consist of all high quality, low risk, low yield investments, whereas, other portfolios might have fixed income investments of lower quality, higher risk and higher yields, or possibly none at all. Any way one wants to look at fixed income investments, they do add a degree of stability to an investment portfolio against economic fluctuations, and they generally do follow the relationship of the return being proportional to the risk.

Bonds

The first thing that comes to mind when most people think of types of fixed income investments is bonds. A bond is a marketable fixed-interest debt obligation commonly issued as a loan by governments or corporations. A bond consists of principal (the face value possibly at a premium or a discount), a fixed interest rate, and a maturity date (the day that it can be redeemed).

Bonds are rated by various investment services, such as, Moody’s, and Standard & Poor’s. These two services use a letter based system that rates the highest quality bonds as Aaa or AAA, best quality, to the lowest quality bonds as C or D, bonds in default.

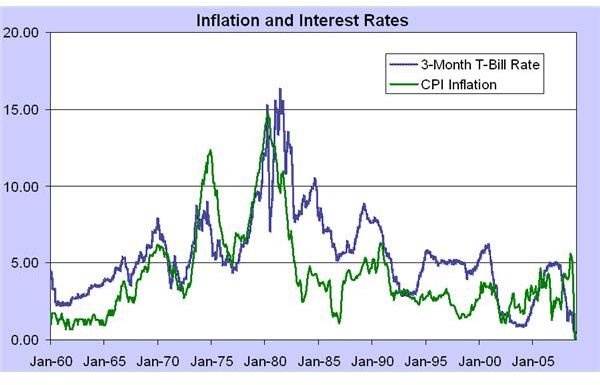

Bonds are susceptible to inflation which eats away at their incomes as interest rates rise. Occasionally buying and selling short-term bonds to adjust for inflation increases is one method used to combat this problem. Another method is to buy bonds issued by foreign governments with stronger economies. This has its own risk though; governments can default on debt obligations just like corporations, and can also become unexpectedly destabilized.

US Treasuries

U.S. government debt obligations, also known as Treasuries, are considered the gold standard for investing because the risk of a default is the lowest, if not nonexistent, of all other marketable securities. They are classified according to their length of time to maturity. Three kinds of government debt obligations that pay a fixed income are:

Treasury Notes (T-notes)

Treasury notes are debt obligations that carry maturity dates of one to ten years. Their interest rate is fixed and is paid every six months. T-notes can be purchased at a bank or at a government auction. The yields when they are purchased vary with the economic times. In the year 1990 ten year T-note yields got as high as 9.09% and as low as 2.08% in 2008.

Treasury Bonds (T-bonds)

Treasury bonds are a government debt obligation that carries a maturity date that is twenty to thirty years. They are issued quarterly and pay interest twice a year. T-bond yields have been as high as 9.17% in 1990 and low as 2.53% in 2008.

Treasury Inflation-Protected Securities (TIPS)

Treasury inflation-protected securities are government debt obligations that adjust the principal against the Consumer Price Index (CPI) while the coupon rate remains constant. The interest payments change with the CPI due to this calculation and are protection against inflation that eats away at most bond incomes.

Treasuries are considered the safest of bond investments. The low interest is also accompanied by low interest rates, or coupon rates which mean that they could be overpriced if demand for them becomes high. The upside for many investors is that income from Treasuries is taxable by the Federal Government but is not taxed by cities and states .

Corporate Bonds

Corporate bonds range in quality from the very high quality “investment grade” bonds to the very low quality, sometimes misnamed, “junk bonds”. Corporates are considered higher risk than Treasuries and this is reflected in their higher interest rates.

Investment quality corporate bonds are usually the conservative choice for those wanting a higher fixed income than Treasuries offer and are willing to tolerate the higher risk. Junk bonds can be a good addition to a protfolio during times of a rising economy due to the fact that defaults are less likely. As with all bonds, both can have their returns reduced by inflation.

Preferred Stocks

Preferred stocks are issues that can be thought of as a hybrid of bonds and common stocks. There are many varieties of them. They pay a fixed dividend that is a percentage of the par value, or the value that is on the face of the instrument, like a bond, and they also appreciate like a common stock. These stocks don’t have voting rights but the dividends are received before, or have preference over, the common stock dividends. They also have preference over common stockholders if the company must liquidate, which means that preferred stockholders have a better chance of getting back their investment than common stockholders, but, being equities, they are subordinate to the senior debt of bonds.

Preferred stock dividends are distributed at the discretion of the company’s directors like common stock dividends, not as a debt obligation like bonds. A dividend could be skipped if the company suddenly found itself strapped for cash, but it might not be lost; this would depend upon the stock being cumulative or noncumulative. Yields are also higher than bonds, common stock, and money market yields.

Dividend Stocks

Common stocks are often purchased for appreciation value but they also can pay dividends to the shareholders similar to preferred stocks. The timing and the amount of these distributions are determined solely at the discretion of the company’s directors. A history of consistent dividend distributions with a low payout ratio (dividend per share divided by earnings per share) indicates stability to an investor. Entering a reasonable criteria into a stock screener can probably bring up some stocks that are good candidates for a fixed income investor to research further and possibly find some investment gems.

Mutual Funds and Exchange Traded Funds (ETF)

Mutual funds and exchange traded funds (ETF) are both managed funds and both can consist of almost any kind of security mix or specialty. They have differences that set mutual funds apart from ETFs.

Mutual funds are strategy based collections of securities that have objectives like low risk, aggressive, growth and other various investment strategies. Their diversification makes them a convenient choice for investors who would rather not attempt diversifying their own portfolios. Mutual fund managers are supposed to generate profits with their expertise but few mutual funds actually beat the market averages. Quite often this is attributed to lower risk which translates to a less worrisome night’s sleep for many investment risk phobics. Managers also take a portion of the fund’s profits, and a monthly management fee is charged whether or not a profit is generated by the fund. Mutual fund fees are based on four elements, sales charges, expense ratios, transaction commissions, and redemption fees.

Exchange traded funds are similar to mutual funds in that they are a collection of assets, but ETFs can consist of different asset classes or the assets can be quite alike as in a bond ETF. The funds aren’t based on a strategy with an objective like mutual funds but are arranged to closely follow an index like the S&P 500 or the DJIA. They also have fund managers whose job it is to keep the fund on the right track.

ETFs are cheaper to maintain than mutual funds. This is due to low expense ratios and they can be traded on the stock exchanges just like stocks using the services of a broker and paying the same commissions. There are many varieties of ETFs trading on the markets numbering in the hundreds (956 are recorded at MasterData on 10/2/2010). There could be something worthwhile there in the area of fixed income investments (bonds for sure).

There quite a few fixed income investments for an investor to choose from. What is considered worthwhile is a matter on one’s own personal propensity for tolerating risk. They all follow that old familiar relationship of risk/reward. The higher the returns, the higher the investment risks.

References

James E. McWhinney, “Why ETFs Are A-OK,” Articles, 2010. Investopedia. Retrieved October 25, 2010 from the World Wide Web: https://www.investopedia.com/articles/mutualfund/05/060605.asp

Undisclosed, “Junk Bonds: Everything You Need to Know,” Articles, 2010. Investopedia. Retrieved October 25, 2010 from the World Wide Web: https://www.investopedia.com/articles/02/052202.asp

Undisclosed, “Preferred Stocks and the S&P U.S. Preferred Stock Index.” Preferred Stock Primer, 2009, Standard & Poor’s. Retrieved Ocotber 25, 2010 from the World Wide Web: https://www2.standardandpoors.com/spf/pdf/index/Preferred _Stock_Primer_2009.pdf?vregion=us&vlang=en

Ben McClure, “Dividend Yield for the Downturn,” Articles, 2010. Investopedia. Retrieved October 25, 2010 from the World Wide Web: https://www.investopedia.com/articles/stocks/09/dividend-yield-for-the-downturn.asp

Images: Public domain, 2010. Wikimedia. Retrieved October 25, 2010 from the World Wide Web: https://www.wikipedia.com/