Sold stocks or bonds for less than you paid for them? Chances are good that it happened at least once last year (maybe lots) for most investors. A capital loss can provide a good tax deduction but there are important rules to understand.

Capital Losses

A capital loss occurs when selling an asset for less than its cost, or basis. In its simplest form, an investment’s basis is the amount that the investor paid for it including any costs directly associated with its acquisition.

For example, when purchasing stock, a broker’s commission is added to the purchase price for the purposes of calculating basis because it is a direct expense to that transaction. This is in contrast to a fee based on the amount of assets in the account. In this case, the fee applies not only to the transaction in question, but to all of the other assets as well. While this fee may be deductible in another way, it is not added to the basis.

When the asset is sold, the difference of the proceeds from the sale determines the amount of the gain or loss. For example, if an investor bought 1000 shares of Microsoft stock for $50 per share with a $200 commission, the basis is $50,200. If the investor then sells the 1000 shares for $40 per share, again with a $200 commission, then the proceeds are $39,800 ($40/share * 1000 shares - $200). The capital loss is therefore $50,200 - $39,800 = $10,400.

Capital Loss Income Tax Deduction

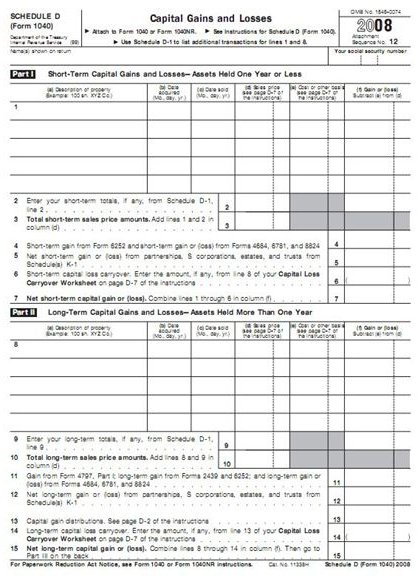

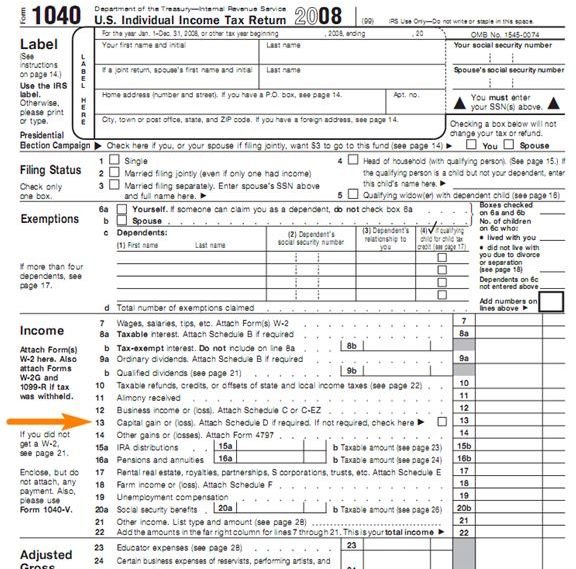

Deducting a capital loss is done on Schedule D of Form 1040. All transactions resulting in a gain or loss are entered on Schedule D. If the net result of these transactions is a negative number, or a loss, then that amount is entered on Line 13 of Form 1040. This results in a reduction of income subject to the limits detailed below.

However, be sure that your numbers do not including any deduction disallowed by wash sale rules .

Capital Loss Tax Deduction Limit

The tax treatment of losses is easy to understand once the basics have been grasped.

While capital losses may be used with no limits to reduce capital gains, the amount by which ordinary income may be reduced by capital losses is limited to $3,000 (or $1,500 each if married filing separately). Thus, the amount entered on Line 13 of Form 1040 may not exceed $3,000 regardless of the total amount lost for the year.

Any loss which exceeds $3,000 may be “carried forward” to subsequent years.

For example, if an investor has a capital loss of $10,000 for the year, only $3,000 of that loss may be deducted on that year’s taxes. The remaining $7,000 may be carried forward. Thus, if the investor has a net gain in the following year of $6,000 the carried forward loss of $7,000 may be applied to that gain resulting in a reportable “loss” of $1,000 ($6,000 gain - $7,000 carried forward loss = -$1,000 for Line 13) for that year.

So, it is very important that the investor keep all records and tax forms from the year with the capital loss until the full loss has been written off.

While losing money on an investment is never desirable, the ability to deduct capital losses may at least provide a small amount of compensation for those losses.

Tracking Investment Capital Gains and Losses

Various software programs and websites provide the best tools for tracking capital gains and losses as well as other investment expenses.