The yield curve plots interest rates comparing rates with time to maturity. However, the yield curve is more than a simple graph. The shape and slope of the curve is an indicator of current and future economic conditions.

Bond Market Rates

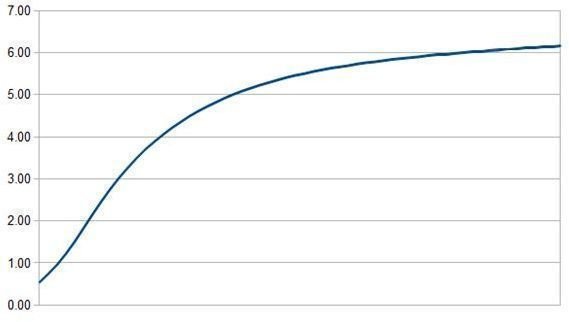

A yield curve involves plotting current market yields against a range of maturities. The yield curve for Treasury securities is the most often discussed and analyzed. Treasuries are the most widely followed debt securities and are available in maturities ranging from 30 days to 30 years at issue. When graphed, the yield curve is shown as a line with the height of the line representing interest rates as maturities get longer. This graph is a sample representation of a yield curve.

Although the simple use of a yield curve is to see where rates are for certain lengths of maturity. The shape and slope of the yield curve can used to get a picture of current economic conditions and where bond market investors believe the economy is headed.

Who Sets Interest Rates?

To understand a Treasury yield curve, you must first have an idea where market interest rates come from. Rates at the short end of the curve, say zero days out to one year, are most influenced by the actions of the Federal Reserve Board. The Fed sets the federal funds rate, which is the rate at which banks can borrow money from other banks and the Federal Reserve Bank. Short term Treasury bill rates will be close to the Fed funds rate.

Long term Treasury bond rates are a function of market supply and demand. Bond investors expect to earn an interest rate that will exceed the expected rate of inflation for the term of the bond. The most widely followed longer term Treasury security is the 10-year note. Up from the 10-year note, the Treasury issues 30-year bonds with no new securities issued with maturities in between.

With the Fed setting the rate for the short end of the yield curve and the auctions of 10 and 30-year Treasuries providing market guidance for rates at those maturities, the rest of the yield curve sort of fills itself in as Treasury bills, notes and bonds of all maturities are purchased and sold on the secondary market.

Curve Shapes

Yield curve analysis is simplified into the shape and slope of the curve when Treasury security yields are plotted against time to maturity. Three yield curve shapes are commonly discussed.

Normal Yield Curve: A normal shaped yield curve has interest rates low at the short end of the curve and gradually increasing to the highest rates at the 30-year end of the curve. This is the most common shape for the curve and makes logical sense. Investors usually expect to be paid a higher rate of interest for locking their money up for a longer period of time. Short maturity securities provide liquidity in exchange for lower rates. The yield curve pictured above is a normal curve. The slope of a normal yield curve, flatter or steeper, can be analyzed as to market expectations for economic growth. Higher growth is expected to lead to inflation, so if high growth is forecast, longer rates will be significantly higher than short rates. Moderate growth does not have as much inflation risk, so longer rates won’t be as high, resulting in a shallower yield curve slope.

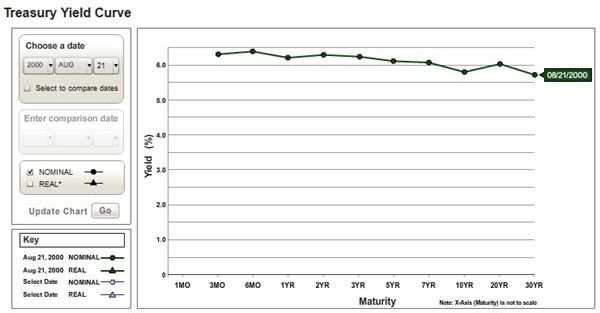

Inverted Yield Curve: When short term rates are higher than long term rates, the yield curve is said to be inverted. Instead of sloping up, the curve slopes down. Rates at the short end of the curve are very high as the Fed tries to slow inflation by increasing short term rates. Long rates are lower than short rate because long term bond investors expect the Fed actions to reduce inflation and interest rates will eventually decline. Long bond investors are happy to lock in rates which are lower than the short rates, but historically high. A recent inverted yield curve occurred in August 2000 (see image) with the 3-month Treasury bill rate at 6.3 percent and the 10 and 30-year rates near 5.7 percent. Probably the most famous inverted curve occurred in 1981, when short term rates were over 15 percent and long bond rates were around 12 percent. An inverted yield curve is viewed as an indicator of a pending economic recession.

Flat Yield Curve: A flat yield curve is when rates are pretty much at the same level from short to long maturities. The curve usually flattens when it is transitioning from normal to inverted or inverted to normal.

Current Treasury Rates

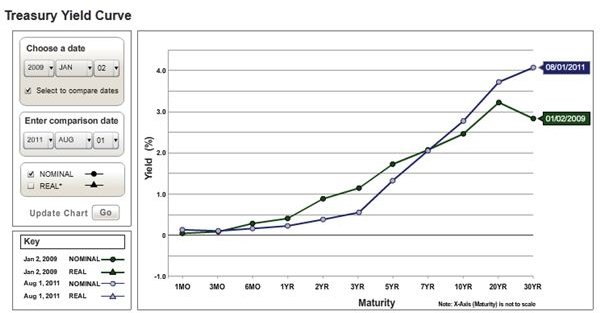

In December 2008, the Federal Reserve Board lowered the federal funds target rate to essentially zero percent. As of end of summer 2011, there is no indication the Fed is ready to again increase interest rates. Economic growth remains sluggish and short term rates have been kept very low to avoid a double-dip recession. Through August of 2011, the yield curve has maintained a positive slope. This is typically an indicator of economic growth, which over this three year period has not materialized. It will be interesting to see what happens to the yield curve when the Fed again believes it is time to increase short term rates.

References

- Milken Institute: Inverted Yield Curves and Financial Institutions; March 2007, http://www.milkeninstitute.org/pdf/InvrtdYieldCurvesRsrchRprt.pdf

- Photo Credits: self-generated using spreadsheet and yield curve diagrams from the Department of the Treasury website.

- U.S. Treasury: Daily Yield Curve Rates, http://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=yield