Ever wondered about the critical factors and actors that have determined crude oil prices for the past century? From European imperialism through the oil shocks to the role played by futures traders today. No commodity is shaped by more factors than the one that fuels the bulk of the global economy.

The Eras of Oil

Oil prices seem to shoot in all directions nowadays. As the global economy’s most vital commodity, even the slightest event can send prices spiraling upward, or, as history has shown time and time again, plunging downwards. Looking into the history and analysis of crude oil prices, the economic factors can be divided into three distinct eras: before OPEC, OPEC dominance, and the age of speculation.

The Early Days

Almost outside of living memory now is the fact that oil replaced coal as the primary fuel source because it was more efficient, and therefore cheaper. Oil became a commodity inordinately entwined with global politics at the time of the First World War. The British Navy, then the largest in the world, switched all of its battleships to oil power during the war. While this made sense from a technological point of view, the decision was made even though Britain did not have any major oil reserves anywhere in its empire. So after the war the political map of the Middle East was redrawn to ensure Britain a steady supply of cheap oil from a set of small countries easily dominated by its foreign sway.

The United States at this time was not only self-sufficient in crude oil but was actually a major exporter. During World War II, Texas and California crude is what kept the Allied war machine rolling whilst the Germans ended up abandoning most of their Panzer tanks for lack of fuel, providing many a GI with a souvenir photo atop a Tiger tank. The Nazis were reduced to synthesizing oil from coal, an expensive, inefficient, and aerial bombing prone process.

Postwar Price Stability

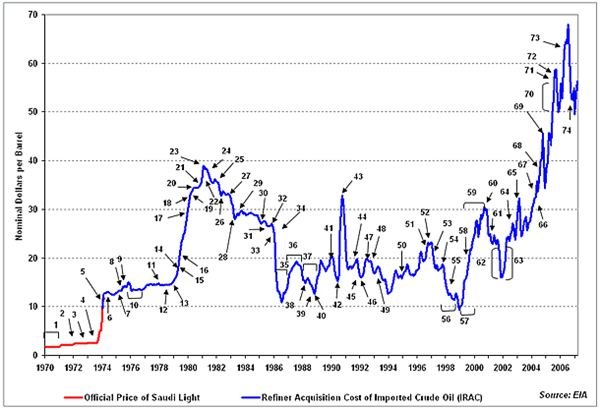

Due to the abundant domestic supply and an accommodating set of neighboring exporters, oil prices in the United States remained at under $20 p/b (2008 dollars) from 1879 through 1970. Oil prices were under strict price controls and subsidies, and this helped American consumers enjoy consistently cheaper oil prices that the rest of the world over the same period, which averaged about $30 p/b during the same period. Yet in the 20 years following the Second World War, the USA went from being an oil exporter to an importer of 47% of its needs.

The Exporters Strike Back

While OPEC is largely considered to be an Arab organization, the true impetus behind its formation in 1960 was the USA limiting Venezuela’s oil exports to the USA in favor of Mexican and Canadian supplies. It was Venezuelan President Romulo Betancourt who led the drive to form an international cartel that would set an agreed price to be shared among members and export quota to set for each member state. The first five members were Iran, Iraq, Kuwait, Saudi Arabia and Venezuela, joined in 1971 by Qatar, Indonesia, Libya, United Arab Emirates, Algeria and Nigeria. It took the new organization about a decade to be felt on the world market, but when it did it produced the Oil Shock of 1974.

Most people believe the massive price hike (OPEC members quadrupled the cost per barrel literally overnight) was purely a reaction to American support of Israel in the 1973 Yom Kippur War. It was also a reaction to long term macroeconomic trends. Even though oil prices remained stable from the mid-60s at the then-price of $3 p/b, in real terms oil exporters were losing money due to high inflationary shocks such as the USA going off the gold standard in 1971. In that same year, American oilfields were permitted to pump at 100% capacity, ending the USA’s ability to maintain spare capacity, essentially surrendering control of global oil prices to OPEC. The 1974 debacle was followed by a short period of price stability, and then the highest spike to date, the 1979 crisis was brought about when the Iranian Revolution removed two million barrels a day from the world market. Saddam Hussein’s invasion of Iran shortly thereafter crippled both countries’ exports (neither has yet matched peak prewar production), while other OPEC members initiated another round of price hikes, leading to a peak of about $120 p/b in today’s dollars.

Postwar Crude Oil Prices

And Then Quickly Fade Away…

Aside from the 1970s oil shocks, OPEC has been consistently unsuccessful at its stated goal. The organization does not have any agency to enforce quotas between members, and the only member with enough spare production capacity to impact global supply is Saudi Arabia. The ‘‘Oil Glut’’ of the 1980s was a result of increased production by non-OPEC members, and the fact that USA oil imports dropped from 47% of national consumption to 28%. This is attributable to the fact that OPEC overplayed its hand. Higher prices led to improved energy efficiency. When demand dropped, attempts to raise prices by imposing production quotas failed as non-members simply produced more. Later, during the early 2000’s price surge, OPEC failed to reduce prices by releasing enough spare capacity.

New Price Movers on the Block

Crude oil prices plummeted to less than $10 a barrel in 1986. The downward trend continued until 1994, except for a brief spike during the First Gulf War. The increasing demand since then is partly explained by macroeconomic factors. Most notably, the developing world required increased oil use in the 21st century. But what really differentiates this as the post-OPEC era is that the price of oil is not primarily determined by either market forces or the cartel, but by the futures market. Oil futures were first traded on the New York Mercantile Exchange in 1983. This put the price of oil into the hands of the speculators, who introduced the ‘‘risk premium’’, or the extra value tacked onto a commodity due to the risk of interruptions, into futures pricing. In a nutshell, a future is a position in which a speculator can either bet a commodity goes up (long position) or down (short position). The previous history and analysis of crude oil prices of all of the previous price spikes were due to simple market factors like supply and demand, or price fixing by political entities.

Futures Make the Peaks and Troughs

But considering that oil essentially fuels civilization as we know it, even the slightest twitch now sends crude prices upward. The speculative surge led to oil prices reaching $147 p/b in 2008. The thing with futures contracts is, the type of contracts being taken out affects their price. If a vast majority of speculators go long, the sheer demand for long position oil futures drives the market price upwards fueling a bubble, which will burst once investors close their positions and take their profits. The 2008 bubble burst as profit harvest occurred. The price dropped to around $40 p/b by the end of 2008 then it started working its way up again, climbing steadily until hitting the $80 p/b mark in 2010. The volatility of oil futures remains high, the price shooting up nearly $20 a barrel amid the latest round of Middle East instability. As of the summer of 2011, it sits at $90 p/b.

The history and analysis of crude oil prices shows that human induced change is the norm. There has never been a actual shortage of oil in the ground, just interruptions in supply and trade imbalances. There are enough untapped oil fields out there to keep us going yet. In fact, many analysts believe that were it not for the cyclical upward speculative pressure, oil would currently sell at about $40 p/b.

References

WTRG.com, https://www.wtrg.com/prices.htm Author Unkown

Economy Watch, https://www.economywatch.com/world-industries/oil/historical-prices.html Author Unknown

Photo credits: Wikimedia Commons

Battleship HMS Ramillies circa 1920, photographer unknown. This is a press photograph from the George Grantham Bain collection , which was purchased by the Library of Congress in 1948. According to the library, there are no known restrictions on the use of these photos.

Oil price chronology.gif, first uploaded by Stirling Newberry, Permissions: PD-LAYOUT; PD-USGOV.