Most of us want to know all the risks involved with an investment before putting up hard earned cash to invest. The types of risk in a Modern Portfolio Theory include a broad, comprehensive list that doesn’t miss anything.

Most investors are risk-averse and any of them would want to construct a portfolio that is optimized for high returns and low risk. Many investment strategies have been devised to attain this goal and the most influential and popular is Modern Portfolio Theory (MPT). Two broad categories of risk were created and help in the theory’s goal of creating a portfolio that is optimized between levels of risk and returns.

About the Theory

The Modern Portfolio Theory was developed by the economist Harry Markowitz and published in the Journal of Finance in 1952. The basic tenet of this theory is that instead of trying to find a single security that possesses an optimized risk/return trade off, that is offering the lowest risk with the highest return, a portfolio could be created that diversifies away the risk for higher returns . This could basically be summarized in the old adage, “Don’t keep all your eggs in one basket.”

What Are the Risks?

Every one knows what risk is and there is actually a certain amount of it involved in everything that we do; it can be remote or very high. This is also true for investing. Any investment has risks connected to it that can affect its performance. Even U.S. treasuries that are considered risk-free are not completely exempt from this. Any government can default on a debt due to various reasons and reasons range from a weakened economy to an extremely debilitating political unrest to global wars.

The Modern Portfolio Theory tries to identify what the risks are for investing and how to best deal with them while maximizing returns. Risks are divided into two broad, fundamental categories, systematic risk and unsystematic risk .

Systematic Risk

Systematic risk is a risk that can’t be avoided or protected from and affects a large number of assets. Examples of systematic risk would be:

- Interest rates

- Weather

- Civil or foreign wars

- Recessions

Unsystematic Risk

Unsystematic risks are events or occurrences affecting a single asset or a small number of them and is also called “specific risk.” This kind of risk can be minimized or eliminated by diversification. Examples of this would be:

- Employee strikes

- Bankruptcies

- Defaults on debts and lowered credit ratings

- Unexpectedly dismal earnings reports

More Considerations

Other risks investors should be aware of include:

Country risk - This is usually associated with emerging markets. It’s the ability of a nation to pay it’s obligations and avoid defaulting on them. This can be contagious for all of the surrounding countries and beyond. This occurred in the summer of 1997 when the Thai Baht depreciated and the Korean Won followed eventually causing a dramatic bailout of investors in the region eventually spreading to nations in Europe and Latin America.

Market risk - This is the potential to experience losses during daily market fluctuations, or volatility, of a security or group of securities. Little attention is given to the causes of the fluctuations than to their effect on prices. The volatility of a security is a systematic risk and is expressed as a term known as beta (ß). Beta is usually a current measure as a securities volatility itself can fluctuate over long periods of time.

Foreign exchange risk -This arises from fluctuating exchange rates when investing in assets that are valued in a foreign currency. Losses can be experienced when an assets’ value rises in price but the value of the currency experiences a decline in relation to the investor’s domestic currency.

Interest rate risk - Here, a security’s value can change with a fluctuation in interest rates. Bond prices drop when Inflation increases providing a discount to investors to make up for the difference between the bond’s interest rate and the higher interest rates caused by inflation.

Political risk - The risk of changing governments and policy changes can create a higher risk investment environment. This is the reason investors stay away from developing countries.

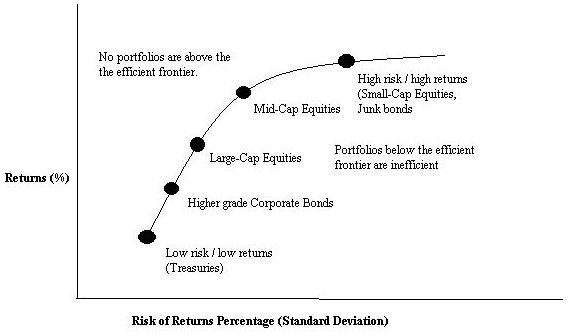

The Efficient Frontier

The efficient frontier was developed while trying to find the optimal risk/return level of diversification for a portfolio. It’s displayed on a graph that uses the percentage rate of return as the Y-axis and the percentage risk (standard deviation) of returns as the X-axis. Portfolios are plotted on the graph beginning with low risk portfolios and gradually increasing in risk to the higher risk portfolios. This graph shows the highest rate of return for each level of risk, and the lowest risk for each level of return. Every portfolio that is on the line of the graph is considered efficient (highest returns relative to the risk) and portfolios below the line are considered inefficient (low returns for high risk). No portfolios exist above the line of the graph as it’s generally accepted that no one would be offering an investment with high returns for a low amount of risk or risk-free and be expecting a profit. The graph below illustrates this (click to enlarge):

The types of risk in the Modern Portfolio Theory showed creating an investment portfolio involved finding the right mix of securities for consistent returns and that it was possible to find an optimal combination of them to fit an investor’s risk tolerance. The two fundamental categories of risk, systematic risk and unsystematic risk are broad and include a number of important risk factors that should not be ignored when considering an investment for a portfolio.

References

-

McClure, Ben, “Modern Portfolio Theory: Why It’s Still Hip,” Investopedia, 2006. http://www.investopedia.com/articles/06/MPT.asp#axzz1QJzARdtM

AdvertisementCarther, Shauna, “Achieving Optimal Asset Allocation,” Investopedia, 2009. http://www.investopedia.com/articles/pf/05/061505.asp#axzz1QbpCdMK3

Steiner, Sheyna, “Buy-and-hold investing not dead after all,” Bankrate.com, 2009. http://www.bankrate.com/finance/financial-literacy/buy-and-hold-investing-not-dead-after-all-1.aspx

AdvertisementLamb, Katrina, “Investing In Emerging Market Debt,” Investopedia, 2010. http://www.investopedia.com/articles/bonds/07/emerging-market-debt.asp#axzz1Qh7slUbE

Images:

AdvertisementEfficient Frontier: Rendering by Bruce Tintelnot

Image: digitalart / FreeDigitalPhotos.net http://www.freedigitalphotos.net/images/view_photog.php?photogid=2280

Advertisement