Inflation is a big issue with most investors. Where can someone invest to keep from eroding their hard earned money and profits? Here, the question, “How do investors deal with inflation?” is answered along with some things to consider in potential investments.

The “worst tax” is an expression that is referred to quite often for describing inflation. It can eat away at the value of investment portfolios, business earnings, or any amount of idle cash without many people even noticing it. Whether it’s creeping inflation that can be adjusted for periodically or a sudden sustained increase that can leave an economy reeling, investors are always looking for places to put their money as a hedge against inflation that yields higher rates of return than the current rate. So how do investors deal with inflation?

What is Inflation?

Inflation is a general rise in prices across the board for goods and services. It’s measured by the Consumer Price Index (CPI) and the Producer Price Index (PPI). The CPI measures cost increases of goods and services from the perspective of the consumers and is followed by most investors, whereas, the PPI measures cost increases of goods and services from the seller’s perspective. The Bureau of Labor Statistics has data for both of these indicators.

Another indicator that is considered more accurate for judging the state of the economy is the CPI food and energy prices. Some favor this over the regular CPI because it removes the volatility of two products that can inordinately affect the economy in relation to the prices of the other goods and services.

These are quite important indicators for investors to be observing when dealing with inflation.

The Causes of Inflation

There isn’t one single cause for inflation. It’s generally agreed upon by economists that it can be caused by the demand for goods and services out-pacing the supply, or when a company’s costs increase and they get passed on to the consumers as price increases.

A certain amount of inflation is actually a part of the economic business cycle that accompanies a growing economy. A reduction in the inflation rate would indicate a weakening economy, and no inflation would result in an economy that’s stagnating and could possibly slide into deflation.

For Investors

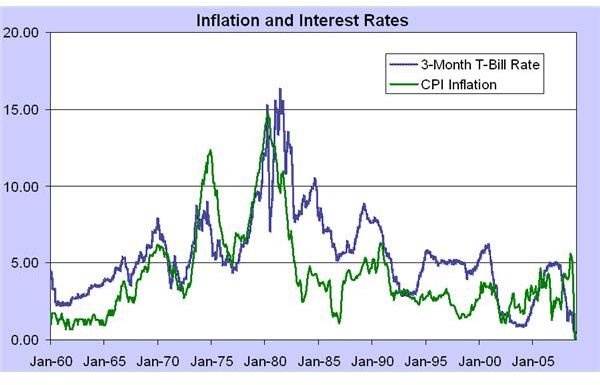

The investments that are hardest hit by inflation are the conservative fixed-income investments, such as, savings accounts, CDs, and bonds. If an investor buys a 10-year bond for $100 at a 5% interest rate (nominal interest rate) with a 3% rate of inflation, the actual annual return (real interest rate) on the investment is only 2% (5% - 3%). The bond can make up for this by lowering its purchase price to $97 but an investor that is holding it for a full 10 years is still losing money during the inflationary period. This disparity can be worse for savings accounts and CDs because their lower amount of risk gives them lower interest rates than bonds.

Stocks don’t fare as badly as fixed-income investments because companies are usually making adjustments for inflation but there still are some problems. One of them would be how a company’s financial statements are affected by the valuation method selected for its inventories during an inflationary period. An inventory valuation method known as first in, first out (FIFO) assumes the oldest items in inventory are sold first can be used for calculating the cost of goods sold (COGS). An inventory valuation method known as last in, first out (LIFO) that assumes the last items placed in inventory are sold first when calculating the COGS. The FIFO method would produce a smaller profit on the financial statements when subtracted from sales revenues because older items of inventory probably experience a lower inflation rate than the most recent items in stock. Financial statements usually mention the inventory valuation method they have used in a footnote.

Companies that keep unnecessarily large amounts of idle cash for long periods of time can also lose value to inflation for obvious reasons that have already been mentioned. This is like keeping your money in a shoe box or a cookie jar. It doesn’t appreciate and it’s probably earning little if any interest while it’s value is shrinking. There could also be interest payments to maintain debt that provided cash for the account.

Possible Investments

No matter what the cause of inflation happens to be, most investors realize they must find places to invest their hard earned dollars that will preserve their capital and provide a rate of return and investment growth that’s higher than the current inflation rate. Usually investing for the long term is how investors deal with inflation.

Fixed-income investments - As mentioned before, these investments are the most vulnerable to inflation. A strategy used for

treasury bills is to sell the bills every 3 months after purchasing them and buy new ones at a more recently adjusted interest rate.

Some fixed-income securities are designed specifically to deal with inflation. A few of them are inflation-protected securities (IPS) usually issued by governments, inflation-linked certificates of deposit, corporate inflation-linked securities, and inflation-linked savings bonds. These are not all set up in exactly the same way.

Stocks - Are riskier than fixed-income securities but can experience the greatest gains against inflation. Some things to look for when considering a company to invest in are high profit margins and a history of weathering changes in the economy. Dividends can also be very important in bolstering a stock’s rate of return against inflation.

Stock investments can be in various forms. An investor can invest directly in a company’s stock on one of the exchanges through a broker or he can invest in many companies by purchasing shares or units in mutual funds or exchange traded funds (ETFs). All of these have fees and charges that can affect an investments returns; investors should be aware of them.

Real Estate - This can be a good investment for counteracting the effects of inflation. Despite the occasional real estate bubbles the tendency for land and housing investments is to rise on average over a long number of years. Taking out a fixed rate mortgage loan is much like a free loan when interest rates are rising due to inflation.

Investing Overseas - Investing in companies located in other nations that have stronger economies can be another inflation hedge. As the world population grows, more people are entering the middle-classes and the demand for resources is increasing giving rise to a new worldwide consumerism. Commodity-based economies with higher interest rates and strong trade balances can be good places to find companies worth adding to a portfolio. A good beginning would be to find a nation with lower inflation rates than your own. It is important to know how both nations calculate their inflation rates.

Summary

How do investors deal with inflation? The pace of inflation is very important. A slowly developing, low rate of inflation that can be anticipated accompanies growing economies and allows for periodic adjustments to wages and interest rates. A sudden, fast-paced increase that is sustained for awhile can be much more difficult to cope with. Usually investing for the long-term is the most practical way to deal with inflation as investment prices will have a tendency to average out and gains can be achieved.

References

-

Barry Kaiser, “Inflation-Protected Securities - The Missing Link,” Articles, 2004. Investopedia. Retrieved February 7, 2011 from the World Wide Web: http://www.investopedia.com/articles/04/091504.asp

Sham Gad, “Timeless Ways To Protect Yourself From Inflation,” Articles, 2010. Investopedia. Retrieved February 7, 2011 from the Worldwide Web: http://www.investopedia.com/articles/basics/10/protect-yourself-from-inflation.asp#12972879917011&656x517

AdvertisementAaron Leavitt, “Banc Some Inflation Protection With These Nations,” Stock-Analysis, 2010. Retrieved February 7, 2011 from the World Wide Web: http://www.investopedia.com/articles/basics/10/protect-yourself-from-inflation.asp#12972879917011&656x517

Richard Barrington, CFA ®, “Coping With Inflation Risk,” Articles, 2008. Investopedia. Retrieved February 7, 2011 from the Worldwide Web: http://www.investopedia.com/articles/basics/08/coping-with-inflation-risk.asp

AdvertisementImages:

US Two Dollar Bill Back, Wikimedia Commons/US Government /Clindberg

Advertisement1953 recession in US, Wikimedia Commons /JayHenry

Inflation and Interest Rates, Wikimedia Commons/Lawrencekhoo