Do home values appreciate forever? Does a boom always precede a bust? A perspective of historical home value trends helps in understanding how the housing market will perform in the future. Read on to learn more.

About Home Value Trends

Sometimes we learn a lot from history. Perhaps a look at historical home value trends will explain why the housing market behaves in the way it does. According to the Census Bureau, median price for new homes are at the lowest level since 2003 and the housing market is going through a period of negative growth.

A study of the home market trends from the beginning of the century shows an interesting pattern. The housing market doesn’t always go through a boom followed by a bust pattern as is widely believed. In most cases, a stagnant period in which the prices remain stable or increase by a marginal amount follows most of the boom years. Often however, prices show a sharp downward trend or a bust. Boom or bust, the market price of homes always stabilize. The House Price Index, which is a measure of average price changes in repeat sales of single family homes, grew at an average of only 5% between the years 1978 and 2003. Thus a historical perspective of home value trends is useful in understanding how the housing market will perform in the future.

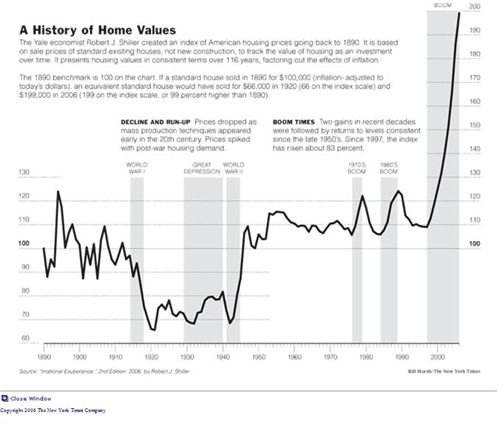

Robert J Shiller, a Yale economist, created an index of American housing prices from the 1890s forward . Although it is only based on the sale prices of existing homes (new construction was not considered), it gives an idea of historical home market trends over the years. According to the graph, a house which sold for $100,000 in 1890, would have sold for $66,000 in 1920 and $199,000 in 2006.

An Analysis of Home Market Trends Over the Years

Although not perfect, Shiller’s graph provides an overall view of the housing market and the range in appreciation value of homes in the twentieth and twenty-first century. Though there are numerous upward and downward spikes, the graph shows only two significant deviations from the median value . One is the bottoming out of market in the 1920s when the prices of houses dropped due to the introduction of mass production techniques after the first world war. Prices remained low throughout the Great Depression and perked up only after the World War II, when returning soldiers from the war increased demand for housing and brought back the home values to the median level.

The second major deviation from the median value is very recent. The value of homes has been appreciating since 1997 and the graph show a sharp ascent during that time. Shiller’s graph is only up to 2006, so it does not reflect the recent market upheaval. It can be suggested that Alan Greenspan’s policy of loosening the credit markets contributed significantly to the boom and the later bust. The emergence of sub-prime mortgage lending in the 1990s enabled a lot of Americans, who would not have qualified for a conventional loan, to own a home. However when the economy fell through, the same people were not able to repay their loans, leading to delinquency and foreclosure.

The Schiller’s graph is a useful tool in analyzing the price appreciation of homes and offers a good historical perspective of home value trends.

Major Factors Affecting Value Appreciation of Homes

A perspective of historical home value trends is helpful in identifying the factors that affect the appreciation value of homes. The overall health of the economy, state of local economy, job market situation, unemployment rates, and long-term interest rates are all factors that affect the price of a home. Historically, the housing market has grown whenever the economy was in good shape. In a growing economy, yields from the stock market put more money in the hands of investors and an expanding job market instills confidence. Also, people tend to put off big investment decisions like buying a home when they are unsure of their jobs.

In addition to the national economy, the local economy also plays a significant role. Home prices can fall when a major industry in the area closes down or starts laying off people. For example in Peoria, Illinois, where the construction equipment giant Caterpillar is based, job losses and salary cuts during the recession in 1980s led to population outflow and adversely affected the housing market. Similarly, in the oil patch states, the housing market boomed when oil industry flourished. Later, when oil prices plunged, many of the cities saw negative growth in double digits.

Historically, lower long-term interest rates have favored higher appreciation of the value of homes. A home is a long-term investment and lower interest rates result in better returns over a long period of time. Interest rates were low during the early 2000s and this could be one of the many reasons why some cities saw the value of homes appreciating by as much as 20 to 25 percent. Looking back, it was a folly to expect that home values would continue to appreciate at that rate forever. That is why a perspective of historical home value trends is so important, one learns that good times don’t last forever.

Resources

1. Federal Deposit Insurance Corporation Website - www.fdic.gov/bank/analytical/fyi/2005/021005fyi.html

2. New York Times Economix Blog - https://economix.blogs.nytimes.com/2010/06/09/interest-rates-and-the-housing-cycle

Screenshot by Swapna Antony: New York Times(Shiller) https://www.nytimes.com/imagepages/2006/08/26/weekinreview/27leon _graph2.html

Image Credit: https://commons.wikimedia.org/wiki/File:Cshpi-peak _nov09.svg