Who Pays for Unemployment Benefits and What Do Employers Pay?

Who Pays for Unemployment Benefits?

This question can mean either one of these two premises:

(1) Who provides the funds from which the unemployment benefits are derived? Is it the federal government, the state, the employer, or the employee?

(2) Who actually disburses the funds extended as unemployment benefits to the eligible unemployed worker? The actual concern with this issue is which state will process the eligible unemployed worker’s benefits in case of interstate or multiple employers in different states?

The following sections discuss how the funding for The Federal-State Unemployment Compensation (UC) Program is raised and which parties are required to pay unemployment benefits:

The Federal-State Unemployment Compensation (UC) Program

The Federal Unemployment Tax was mandated via the Federal-Unemployment Tax Act (FUTA), and it requires employers to pay (1) a federal unemployment tax and (2) a state unemployment tax.

The tax payments are shouldered by the employer alone and should in no way be deducted or collected from the employees.

(1) The Federal Unemployment Tax

Employers are required to pay 6.2 % on the first $7,000 paid as compensation to each employee for the entire calendar year. The purposes of this federal unemployment tax are the following:

-

Provide the federal government working funds in administering or extending unemployment compensation benefits to eligible employees.

-

Provide funds using part of the tax proceeds for one-half of the cost of unemployment benefits claimed by the eligible employee claimant.

-

Provide funds from which a state can borrow, in case it does not have enough funds to meet the unemployment compensation claims of its eligible employees.

(2) The State Unemployment Compensation (UC) Tax

In addition to the federal unemployment tax, employers are also required to pay State UC taxes to provide unemployment funds to eligible workers.

The tax rate varies in every state because it is based on the state’s unemployment rate at the time of tax filing. It follows, therefore, that if the number of unemployed in a particular state increases, the tax rate for state UC tax also increases; thus the employer‘s tax payment becomes higher.

On the other hand, employers that represent the state sector with low unemployment experience with rates lower than 5.4% are entitled to receive additional credits in their UC contribution fund. Any difference between the taxpayer’s actual UC tax payments against the amount paid if computed at 5.4% will be added as additional credit to the taxpayer’s accumulated Unemployment Compensation fund for the benefit of the employer’s laid-off workers.

(1) Who Provides the Funds for the Unemployment Compensation Benefits?

Based on the above explanations, we are drawn to the conclusion that the answer to this query would be the employer, albeit collected and administered jointly by the federal and state governments.

The Federal-Unemployment Tax Act (FUTA) is actually a system by which employers are forced to set aside funds in order to benefit unemployed workers who were rendered jobless as a result of downsizing or due to unforeseen events or circumstances that rendered the employee unemployed through no fault of his own.

Hence, those who were terminated for cause or who voluntarily resigned from employment are not considered as “eligible unemployed workers.”

The state UC taxes are also referred to as UC contributions and an employer, who is not exempt from paying this contribution, will have to pay penalties, interest and/or special administrative taxes for any failure to remit the UC tax or contribution.

Federal laws also require that the state UC tax will be used only as funds to meet the unemployment compensation benefit claims of eligible unemployed workers.

Please continue on Page 2 for more on Who Pays for Unemployment Benefits?

Continuation: Who Provides the Funds for UC Benefits?

Who are the Employers Being Required to Pay the UC Tax?

-

Employers who paid wages to employees in the amounts of $1,500 or more in any quarter during 2008 and 2009.

-

Employers who had workers under their employment for even a fraction of a day for at least 20 or more different weeks in 2008 and another 20 or more different weeks in 2009. This is regardless of employee status, whether full time, part time, or temporary.

-

Employers who hired household help whether in private homes, in local college clubs, or in a local chapter of a college fraternity or sorority and paid cash wages of $1,000 or more in any quarter of the calendar year for 2008 and 2009.

-

Agricultural employers who paid $20,000 or more as compensation to farm workers in any given quarter of 2008 and 2009.

-

Agricultural employers who employed 10 or more farm workers for even a fraction of the day not necessarily on a per-day head count but on a collective basis for at least 20 different weeks in 2008 and another 20 different weeks in 2009.

Who are the Employers Exempt from Filing and Paying the Federal-Unemployment Tax Act (FUTA)?

-

Employers belonging to a federally recognized tribal government, including its subsidiaries.

-

Employers of tax-exempt organizations like educational institutions, religious organizations, charitable institutions, and other organizations exempt from filing taxes under 501.

(2) Who Disburses the Funds Extended as Unemployment Benefits?

After establishing who provides the funds set-up and administered by the federal and state unemployment offices as unemployment benefits for laid-off workers, we will proceed on how the latter can avail of this benefit.

Problems and confusion usually have been encountered for claims that have been denied and in some cases, they pertained to unemployment compensation benefits involving interstate claims. Thus, in order to furnish the answer, we provide information where the jobless workers could file their appeals as well as the rules regarding interstate claims.

How do Unemployed Workers Make a Claim?

Procedures for filing claims vary from state to state; hence it would be best if the claimant inquires from the State Unemployment Office where he currently resides about his options as well as the procedures and the requirements needed to request unemployment benefits.

Some states, like New York and California, maintain websites where laid-off workers can file online their claims for unemployment compensation benefit.

What are the Premises Considered When Claiming Unemployment Benefits?

The basic rule when filing a claim for unemployment benefits is to file the claim in the state where the place of work is located, regardless of where you are residing.

If several employers from different states are involved, the paying state where the worker is currently qualified as an eligible unemployed worker will assist the individual in claiming his UC benefits from the other states by combining all UC benefits inuring to the jobless worker. The assisting office will in turn refer to the Interstate Benefits Payment Plan to determine the paying state that will address the unemployed worker’s claim.

If upon filing the claimant is still unemployed, the paying state where he is qualified as an eligible unemployed worker would be the state where the claimant had his latest employment.

In a case in which a state denies the claimant his request for combined wage claims, it must provide the latter information as to which state his claims can be made. This is to clear all confusion as to who pays the unemployment benefits claimed by the eligible unemployed worker.

What to Do in Case the Unemployed Worker is Unjustly Denied this Benefit?

The State Unemployment Office of the Department of Labor gives emphasis that any failure to assist the disadvantaged worker is considered as unfair to the worker for whom the Unemployment Compensation program was created, as well as to the employer who was mandated to provide the funds for the said program.

For any denial issues that the unemployed worker wishes to appeal and forward to the State’s Unemployment Office, claimants may refer to the Department of Labor and Workforce Development website –Appeal Rights to determine the steps to be taken when filing appeals.

Reference Materials & Image Credit Section

Reference Materials:

- Employment and Training Administration — https://workforcesecurity.doleta.gov/unemploy/laws.asp#InterstateAgreements

- Interstate Benefits Payment Plan — https://workforcesecurity.doleta.gov/unemploy/pdf/istate_agree_bene_payment.pdf

- Federal-State Unemployment Compensation (UC) Program — https://www.regulations.gov/search/Regs/home.html#documentDetail?id=0900006480774160

- Appeal Rights — https://lwd.dol.state.nj.us/labor/ui/aftrfile/appeals.html

Image Credits:

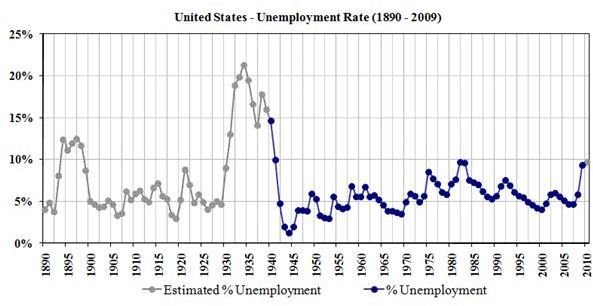

- US_Unemployment_1890-2009

- Workers unemployed by the freeze in California

- UnemployedatQueensParkToronto.

- Helpende Hand-vrywilliger

- [Photograph by Win Henderson taken on 10-08-2005 in Louisiana.jpg](/tools/Photograph by Win Henderson taken on 10-08-2005 in Louisiana.jpg)