What Is the Gross Margin Formula? Explaining With Examples

A Quick Performance Gauge

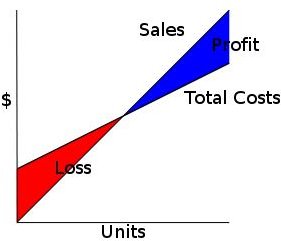

Gross margin is gross profit expressed in terms of percentage or ratio. The percentage is applied to determine how much of the money generated by the business activity is available for operating expenses, interest expenses, and, ideally, returns on stockholders’ investments.

In knowing how to compute the gross margin, the business owner will have a quick reference for gauging business performance in real time. This way, he can institute measures to increase sales or to control overhead costs at the earliest time possible.

The gross profit margin formula in order to arrive at the percentage is as follows:

Gross Margin = (Gross Revenue – Cost of Goods Sold) / Gross Revenue

To illustrate as example, consider the following givens: Gross Revenue (GR): $50,000; Cost of Goods Sold (COGS): $10,000

Gross Margin = ($50,000 - $10,000)/$50,000

= $40,000/$50,000

= $0.80 or 80%

This means, for every dollar of the $50,000 gross revenue earned, $0.80 can be used to pay for operating expenses and partly for distribution of returns on stockholders’ investments. The $40,000 amount in this quick computation is aptly called the Gross Profit when presented in the Income Statement.

What is the Significance of Gross Margin Percentage?

Determining the gross margin percentage of the business operations takes away the notion that profitability can be determined only after the entire accounting cycle has been completed. The gross margin percentage is a profitability tool one can use in today’s proactive trend in business management.

A quarterly review of business performance, for example, will allow management to determine if the business is currently generating enough sales to pay for the usual business expenses incurred in its business activities.

There are several factors to consider when making a review of your business’s current showing in terms of gross profit margin:

1. The current gross profit should be more than enough to pay for the fixed costs. Bear in mind that some expenses like rent and salaries represent fixed costs and will not be dependent on the quantity of goods sold.

2. The greater the amount of gross profit realized, the higher the possibility of paying the investors some rate of return on their investments after satisfying all operating expenses.

3. A gross margin that is almost equivalent to what you are currently spending for operational expenses means you are only meeting the break-even point.

4. A gross margin that is too low and not enough to cover even the operational costs means the business trend will have to face recovery first before it can realize profit. This means the business is unable to recover part of the money that was used to procure or manufacture the goods for resale.

Areas to Consider in Evaluating Gross Margin Percentage

- If a review of the gross margin percentage shows favorable trends, management should consider reviewing products that have high rates of turnovers in order to take advantage of their salability or the demand for the product. Another aspect to consider is the number of staff acting as a sales force or the effort exerted in order to generate sales.

Fixed costs like rent and manpower should be fully harnessed in revenue generation.

-

Budget projections for expenses based on historical costs should be evaluated against the current gross profit margin. Curbing variable costs according to present trends instead of sticking to historical performance will give more realistic uses of gross margin in projecting a favorable net income.

-

Increase in purchase prices of costs of goods sold that tend to lower the gross margin does not necessarily mean increasing the mark-up. Increasing selling prices can possibly slow down the turnover rate, which could lessen the gross margin even more; hence consider the alternative option of reducing your overhead costs.

In order to appreciate the significance of gross margin percentage and its areas of consideration, readers may refer to a separate article entitled Performing a Gross Margin Calculation, where they can find examples and explanations.

Reference Materials and Image Credit Section:

Reference:

- Entrepreneur.com Gross Profit Margin And Markup August 23,2000 —https://www.entrepreneur.com/money/moneymanagement/financialanalysis/article21936.html

Image Credit: