T Accounts: Examples & How They're Used

In accounting transactions and concepts that require multiple entries to record related transactions, it is sometimes necessary to prove the effects of the entries involved before they are finalized as such. This is where the usefulness of T accounts in accounting comes into focus, to serve as a simulation of the general ledger page where the debit and credit entries will be posted.

Others have the misconception that T accounts are tools for proper recoding. Actually, they merely serve as “scratch pads” or working papers in order to prove the effects of accounting entries before they are officially recognized. Others may make use of T accounts to analyze specific accounting data which can be used for business analyses. Examine the examples of T accounts presented below, in order to appreciate their usefulness as a form of “scratch pads” during accounting discussions, deliberations and analyses.

Examples of T Accounts and Their Use in Computing for Gross Profits and Cost of Goods Sold

The Cost of Goods Sold Formula and the effects of its sub-components when presented as accounting entries can be analyzed by using T Accounts. The significance of computing the Cost of Goods sold separately from other cost outlays is a way of determining the Gross Profit of the company. The aim is to determine the margin by which the business can operate in order to realize a favorable bottom line net income. In a scenario where management would like to have a quick overview of the current operational performance of the business, presenting the related general ledger account balances and their anticipated accounting entries via T accounts, can provide the information needed.

To complete the scenario and in order to illustrate the use of T Accounts in accounting, the following given data will be analyzed:

- Merchandise Inventory, Beginning: $ 115,000

- Purchases as of cut-off date: $ 25,000

- Physical Inventory as of cut-off date: $ 70,000

- Total Sales as of cut-off date: $ 87,500

- Total Operating Expenses as of cut-off date: $ 8,000

- Mark-up Rate of Prices on Items Sold: 25%

Accounting Entries Related to the Computation of Cost of Goods Sold and Gross Profit

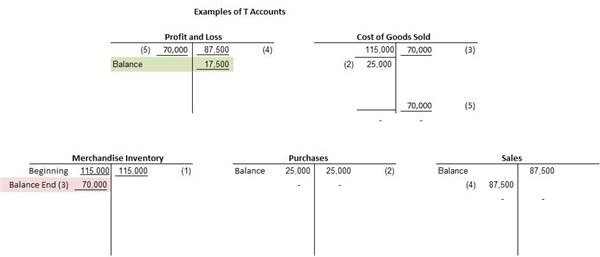

Below are the temporary accounting entries used in order to compute the Cost of Goods Sold and the Gross Profit . These accounting entries were posted in the examples of T accounts on your right, which you can view by clicking on the image.

(1) The Merchandise Inventory Beginning will be recognized as a sub-component of COGS.

Dr. Cost of Goods Sold: $115,000

Cr. Merchandise, Inventory: $115,000

(2) The balance of the Purchases Account as of cut-off date will be recognized as a sub-component of COGS.

Dr. Cost of Goods Sold: $25,000

Cr. Purchase: $25,000

(3) The value of the physical inventory as of cut-off date will be recognized as the new Merchandise Inventory balance and will be deducted from the total cost of goods sold available for sale during the year.

Dr. Merchandise Inventory: $70,000

Cr. Cost of Goods Sold: $70,000

(4) The total Sales as of cut-off date will be reflected in a Profit and Loss T Account.

Dr. Sales: $87,500

Cr. Profit and Loss: $87, 500

(5) The resulting balance of the Cost of Goods Sold will be transferred to the Profit and Loss T Account.

Dr. Profit and Loss: $70,000

Cr. Cost of Goods Sold: $70,000

Discussing the Results Produced by the T Accounts in Accounting

The focus of this T account accounting analysis is the balance produced in the Profit and Loss T account. Based on this, the following information can be derived by management for decision-making purposes:

-

The Profit and Loss T Account shows that the Sales figure of $87,500 posted on the credit (right) side is a higher figure than the $70,000 Cost of Goods Sold (debit/ left side)closed to this account. The resulting balance as of cut-off date is $17,500 which represents the Gross Profit up to this point.

-

In as much as the Total Operating Expenses as of cut-off date amounts to $8,000, a Net Income figure at the time of discussion can be fairly estimated at $9,500 ($ 17,500 - $ 8,000), which means that the business is still enjoying a favorable bottom-line net income in its present operations.

-

However, the Gross Profit Margin that the business is currently working in should be determined in order to analyze if the business is earning enough to compensate for the money tied –up in this investment . If one is to analyze it further, using the Gross Profit formula = Gross Profit/Sales or $17,500 / $ 87,500 = 0.20. This means that for every dollar income realized as Sales, it has $0.20 to show for net profits, based on its markup rate of 25%. Although the gross profit margin is less than 25%, this can still be considered as a good investment option if compared to placing one’s money in a 1-year CD that earns at 3% p.a.

-

However, at a Net Income of $9,500, the earnings per dollar Sales is only $0.11 if all other operating expenses will be deducted from Sales.

-

Based on these examples of T Account accounting analysis, management still has to consider that there is still $70,000 worth of merchandise unsold.Also, some future operating expenses may yet increase; hence, management may decide to increase the selling price at a higher markup than 25%. Another option is to cut down on some of its operating expenses, since increasing the sales price may affect the sale of the remaining merchandise unsold. Management may also consider procuring more stocks to increase the volume of sales by marking-down its selling price. This way, there will be more revenues generated while selling within the same amount of operating expenses being incurred.

This now is an example of T account usage and how it serves as an accounting tool for business decisions, using a set of accounting data for analysis. To know more about T accounts, a separate article entitled Templates for T Accounts will further discuss its use in accounting as well as provide a tutorial on how to create your own T accounts template.

Reference Materials Section

Reference Materials:

- https://www.reallifeaccounting.com/pubs/Article_Theme_Accounting_for_Inventory.pdf

- https://www.investorwords.com/1158/Cost_Of_Goods_Sold.html

- https://www.principlesofaccounting.com/chapter%205.htm