Sample Cash Flow Statements to Illustrate Direct Approach or Reconciliation Method

Understanding the Essence of a Cash Flow Statement

A sample cash flow statement and its corollary balance sheet and income statement are provided in this article in order to furnish the readers with another financial analysis aspect. All three documents comprise the financial reports submitted to the Securities and Exchange Commission to satisfy the federal government’s reportorial requirements .Another document, which is the statement of stockholders’ equity, completes the entire set.

A cash flow statement is actually a tool for financial evaluation, which a financial statement reader can use to gauge the company’s ability to generate cash from its business operation.

Understand that a business venture is considered profitable if its business operation has the capability to recover more than the costs incurred to sustain its transactions. An income statement presents the net income or net loss from operational activities. However, the said report cannot be readily used as the basis for determining if the actual cash increase for a specific period came from operations, and not from loans or stockholders’ investments.

Revenues could be the cash collected at point of sale or could still be partly realizable upon its collection as receivables, in the same way that some of the expenses could have been paid in cash but also partly deferred as payables. This is why the reported net income or net loss is rarely the same amount that increases or decreases the cash position of the company.

In some cases, it is also possible that certain increases in cash balance may have been derived from loans or from investors’ contributions and not actually as a result of profitable business activities. This is now the essence of the cash flow statement as a tool for financial analysis. It presents an overview or a summary of how cash was generated and how cash was utilized during the business cycle.

Study of a Sample Cash Flow Statement as a Tool for Financial Analysis

Actually, our study involves not just one but two examples of cash flow statements because there are two ways by which this financial analysis tool is presented. One method is called the direct approach while the other is known as the reconciliation approach.

Both methods require the balance sheet and income statements as sources of data input. Kindly click on the screenshot images to have an enlarged view, and glean from them the increase or decrease of the account balances. Some of the cells have been color coded so you can readily pinpoint their presentation in the sample cash flow statement, highlighted with the same color.

Example of Cash Flow Statement Using the Direct Approach or Direct Method

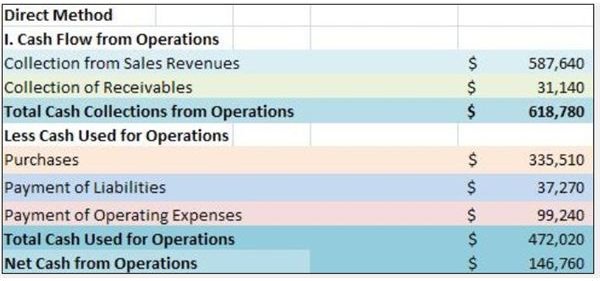

I. Cash Flow from Operations

This section pertains to revenues that were realized as cash from point of sale–to which the amount of cash realized from sales on credit has been added.

Notice however, that the amount for Collection of Receivables made use of the increase or difference between the beginning balance and the balance at the end of the year. A decrease in balance denotes that part of the sales receivables have been collected.

Conversely, if the difference resulted in an increase at the end of the year, the revenue from sales should be adjusted by the said amount. Consider that part of the revenues are yet to be collected as of the report date, hence there is no cash involved. The increase is to be captioned as “Less: Revenue from Credit Sales”

For purposes of illustration, supposing the Amount of $31,140 represents an increase in accounts receivable, Cash Flow from Operations should be presented differently as:

- Collection from Sales Revenues $587,640

- Less: Revenue from Credit Sales $31,140

- Net Cash Collection from Operations $556,500

Please proceed to the next page where we continue with the Sample Cash Flow Statement (Direct Approach).

Example of Cash Flow Statement Using the Direct Approach or Direct Method (continued)

Cash Used For Operations

The ability of an organization to fund all costs related to its operations, using actual cash collected from revenues earned during the period, indicates a capacity for cost recovery. This can be determined by presenting the reductions made against the cash collected from operation, which includes:

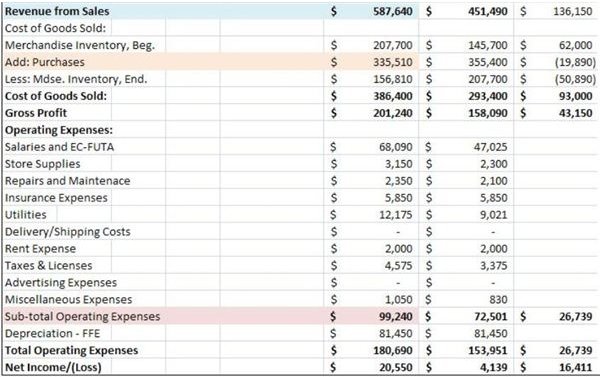

Purchases – Find this amount in the income statement as part of the Cost of Goods Sold presentation.

Operating Expenses – Find this amount also in the income statement but captioned as “Sub-total Operating Expenses”. Depreciation expense has been excluded because it is a non-cash item and therefore has no effect on the cash balance.

Payment of Liabilities – Look for this amount in the balance sheet and, again, take note that the decrease or the difference between the beginning and end balance was used. A decrease denotes payment of obligations related to business activities.

If the difference is an increase, this means that some of the expenses incurred for the operations are yet unpaid. Although we cannot pinpoint whether the unpaid liability relates to purchases or operating expenses, the amount will simply be taken as an adjustment of the cash usage.

After which, the total of these three components is captioned as “Total Cash Used for Operations”. However, if any adjustments are made, use the title “Net Cash Used for Operations “.

Subtract the Total Cash Used for Operations from the Total Cash Collections to determine how much of the cash generated from the business operations remains intact. The amount will have a positive effect on the entity’s cash balance.

If the amount of total cash utilized is higher than the total collection, the negative effect reduces the cash balance and will indicate that the business did not generate enough funds to allow for total cost recovery.

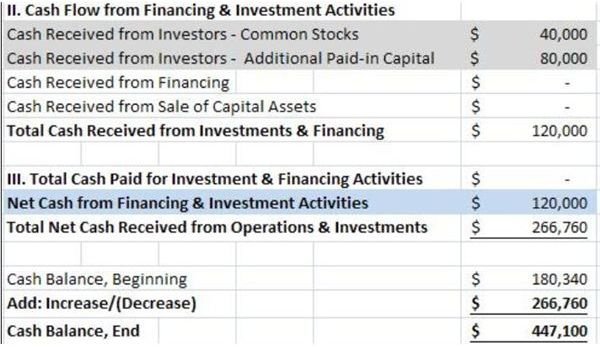

II. Cash Flow from Financing and Investment Activities

The following explanations will now dwell on the second section, which pertains to cash received not as a result of business operations but from other sources like loans, stockholders’ investments or sale of capital assets.

In this study of a sample cash flow statement using the direct method, the entity’s balance sheet does not have any item for long-term loans, hence it can be surmised that the company does not resort to financing activities.

Our next focus will be the stockholders’ equity and, from there, it can be noted that the common stock and the additional paid-in capital increased by $40,000 and $80,000 respectively. This denotes that additional cash funds were received as more investors bought the company’s shares of stock and at prices above the par value.

In the event that the company pays dividends to the stockholders, the amount paid will be presented as a reduction under this section. To illustrate this, we will work on the assumption that a cash dividend of $50,000 was disbursed in favor of the stockholders during the year. In such a case, the cash flow statement’s section for Total Cash Paid for Financing and Investment Activities will include this particular transaction.

The same holds true for other related transactions like repayment of interest and principal on long-term loans, purchase of capital assets, or retirement of bonds.

Reconciling the Total Cash Received with the Changes in Cash Balance

To check the accuracy of the Net Cash Received from Operations and Investments derived, the amount of $266,760 is reconciled against the increment of the cash balance, as reflected in the balance sheet statement.

Nonetheless, the reconciliation is formally presented in the last part of the sample cash flow statement as a standard format and for the convenience of the financial statement reader.

Please proceed to the next page for this article’s explanation of a sample cash flow statement using the Indirect Method or Reconciliation Approach.

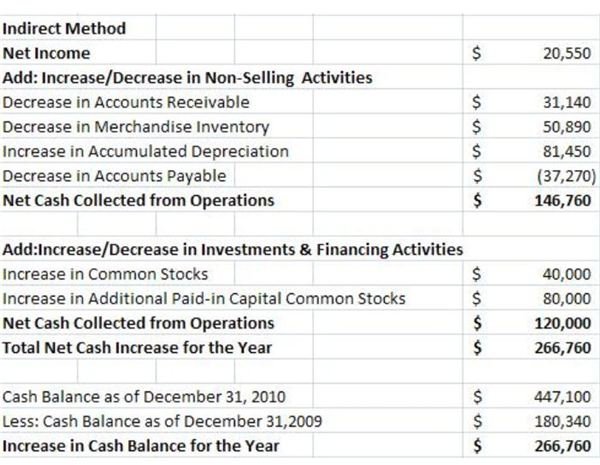

Example of Cash Flow Statement Using the Indirect Method or Reconciliation Approach

This type of presentation utilizes a sample cash flow statement that immediately focuses on the net income as the source of cash.

Net Cash Collected from Operations

Since the net income is the end result of the income statement, the process of establishing the amount of cash collections entails working back from the end point to the beginning. It requires a careful analysis of the increases and decreases in account balances that are affected by cash transactions .

Explanations regarding increments and denouements for accounts receivables and payables are the same as those mentioned for the direct approach. Hence, they are added if the change denotes cash inflow for the business and deducted if it denotes outflow.

The tricky part in this method is the increase or decrease in merchandise inventory. Merchandise inventory beginning represents the goods carried over from previous year, which is $207,700 in the sample balance sheet.

-

Purchases for the year presents cash outflow of only $335,500 but COGS amounted to $386,400; the difference of $50,900 is presumed as derived from previous stocks. The increase, therefore, is rendered as a non-cash transaction.

-

To lessen your confusion in analyzing this cash flow treatment, temporarily disregard the First-in-First-out method of costing, but instead, base the transaction on actual cash outlays as far as cost of goods sold is concerned.

-

Depreciation is a non-cash expense and, therefore, added back to the net income.

-

In the sample cash flow statement, the adjusted net income represents the net cash collected for the year to show cash funding and utilizations from and for operations.

-

After which, the increases or decreases in liability and capital accounts affected by cash transactions are likewise added or deducted accordingly. The final amount represents the Total Net Increase for the Year of $266,760.

In line with the reconciliation approach, the cash balance will likewise be presented from the end balance, and will be reduced by the net increase of $266,760, in order to arrive at the Cash Balance beginning.

Summary:

Based on our study of sample cashflow statements, the financial statement reader can easily determine if the business has a healthy financial condition or not. Cash flow statements that present negative cash collections from operations, are indicative of precarious cash positions. Funding for operations and obligations may have been derived from a non-working capital, from borrowings, from sale of capital asset or from stockholders’ contributions.

Reference:

- Explanations, financial statements, and examples of cash flow statements, as well as the screenshot images, were created for this article by the author.

Image Credit

- Gnucash-account-summary courtesy of GNU General Public License at Wikimedia Commons.