What is a Working Capital Cycle?

Definition

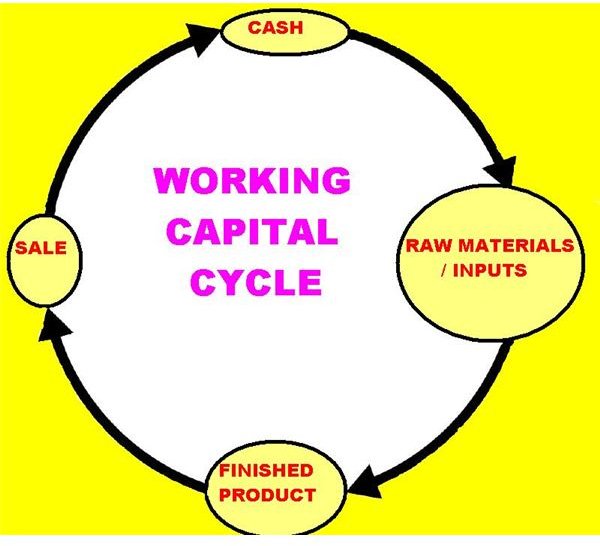

The working capital cycle is the time that elapses between investing in a product or service and receiving payment for that product or service. The starting point of the working capital cycle is usually when the business purchase raw materials or hires people for the service. The ending point of the working capital cycle is when the customer makes the payment, regardless of whether such payment comes pre-paid for the service or purchase, payment takes place at time of purchase or obtaining the service, or the payment comes later owing to sale on credit.

For instance, if a company purchase raw material on day 1, manufactures the product on day 7, and sells it on day 15, receiving payment on day 23, the working capital cycle is 23 days. If the company sells the same product on cash basis, the working capital cycle is 15 days.

A simple working capital cycle illustrates the conversion of cash to raw materials and labor, the raw material and labor to finished products, and the finished products to cash. Failure to move each asset through the cycle continuously leads to a breakdown of the cycle, and with it a liquidity crisis where the company cannot purchase additional raw materials or make payments to sustain its operations. This can lead to a shutdown and even bankruptcy.

Uses

The working capital cycle indicates the time that the company has to block money on the product or service before it gets back the money to manufacture additional products and or reinvest some of the profits from the investment for further growth and research.

A company with short working capital cycle usually has a healthy cash flow, and companies with long working capital cycles usually have cash flow difficulties. A lengthy working capital cycle owing to credit sales mean that the company does not have cash to re-manufacture the product even after selling the manufactured product. To sustain operations, the company then has to deploy additional working capital and manufacture a second batch of items without realizing money for the first batch.

Application

Working capital is actually cash tied up with little or no returns, and as such, companies seek to minimize working capital deployment by shortening the working capital cycle.

Good working capital cycle management seeks to balance incoming and outgoing payments by identifying and synchronizing dates of accounts payable and accounts receivable. This entails identifying points where the company has to make more accounts payable, but does not have adequate accounts receivables to match such payables, and then trying to push back accounts payable or bring forward accounts receivables.

The ideal scenario for a company is to affect a perfect balance between accounts payable and accounts receivable, so that the company can maintain zero working capital and still operate smoothly. Companies such as Amazon collect payment before starting the manufacturing process, and as such maintain negative working capital levels. Other companies delay making payment to suppliers of raw materials until getting payment from customer for the finished goods. Such companies always remain flush with funds, and have zero working capital cycle. Adoption of just in time methodology allows taking this concept even further.

Distorters

Effective management of the working capital cycle depends not just in striking a balance between collecting payments for sales and making payments for raw materials. A company needs working capital for other operational aspects such as rent, paying various taxes, paying dividends to shareholders, making loan repayments and interest obligation, and may other purposes. Most of these items entail a routine and fixed outgo, independent of the product manufacture and sale cycle. Such accounts payables can put a spoke in the working capital cycle, and effective working capital management needs to take due cognizance of such payments.

A good understanding of working capital cycle is the first step towards achieving operational and financial efficiency for a firm.

Reference

QFinance. “Working capital Cycle.” https://www.qfinance.com/contentFiles/QF02/g1xtn5q6/13/2/working-capital-cycle.pdf. Retrieved 12 February 2011.

Image by N Nayab