Examples of Multiple-Step Income Statements: When Should You Use One?

The Uses of the Multiple-Step Income Statement

In a separate discussion of the Income Statement in the article entitled “Income Statements: Free Template and Example”, the single-step format for income reporting purposes was used and the guidelines in its preparation were also provided. In order to complete the explanations on how more complex accounts are presented in case the industry involved is multifaceted, segmented examples of multiple-step Income Statements are herein provided.

Keep in mind that the concept and objectives of the two formatting styles are basically the same; hence, the differences mostly lie on the purpose of their uses. Such uses can be cited in the following aspects:

-

The multiple-step Income Statement format can best serve business entities engaged not only in selling or trading of commodities but also in manufacturing the products being sold. Management will have a more comprehensive basis to measure the efficiency of their business plans and projections.

-

Since the multiple-step Income Statement contains more details, the data used to compute the accounting and managerial ratios applied by internal and external users are easily extracted.

-

Due to the intricacies of the transactions involved in a multi-operational industry, a compartmentalized system of reporting provides easier reference to reconcile errors or reportorial inconsistencies.

-

Revenues from primary activities can be readily distinguished from the revenues of secondary undertakings. Management will have a quick reference to determine the focus for improvements. Secondary activities include investments of idle funds; hence, a clear-cut presentation of this income will allow management to swiftly analyze and decide on the profitability of the investment tools.

-

Presentation of the Gross Profits earned can readily establish profits earned from price mark-ups, since the information will be provided separately before deducting the operating expenses or those that are not directly related in the purchase or manufacture of the goods sold.

-

The components that link the Balance Sheet and the Income Statement can be readily perceived, i.e. Merchandise Inventory as a component of the Cost of Goods Sold presentation and the relationship between sales on credit (Accounts Receivable) to the Revenue from primary activities.

-

The expenses projected in the Cash Flow Statement can be readily analyzed and projected.

An Income Statement for a manufacturing concern is one of the examples of Multiple-Step Income Statement, which can be used to illustrate the formatting style discussed above. You can find samples in Bright Hub’s Media Gallery, Re: (1) Gross Profit Section in a Multiple-Step Income Statement and (2) Net Income After Operating Expenses Section in a Multiple-Step Income Statement. These sectional samples can likewise be used as models to modify a Single-Step Income Statement.

The following are the guidelines on how to prepare a Multiple-Step Income Statement.

Guidelines for a Multiple-Step Income Statement

Basic Information - Please refer to the guidelines provided in the “Income Statements: Free Template and Example.”

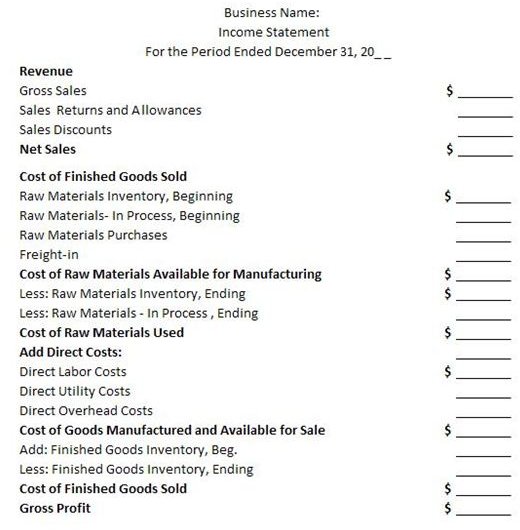

The Gross Profit Section - The image on your right is the Gross Profit section of an Income Statement presented in a Multiple-Step format. Kindly click on the image to enlarge the view.

Gross Sales - This figure represents actual sales transactions consummated for the year without taking into account the amount of returns and refunds made by customers, as well as the sales discounts granted as reduction of the selling price.

Sales Returns and Allowances - This account represents the total value of defective merchandise returned by customers and the resulting discounts granted.

Sales Discounts - Represents the price reduction incentives for sales on credit that were paid ahead of due dates.

Net Sales – The difference after deducting the Sales Returns and Allowance and Sales Discounts from the Gross Sales. The mathematical equation can be expressed as

Net Sales Formula = Gross Sales – (Sales Returns and Allowances + Sales Discounts)

Continue reading on to the next page for the rest of the guidelines of preparing Income Statements using the Multiple-Step presentation.

Continuation of Guidelines for a Multiple-Step Income Statement

Cost of Finished Goods Sold – This section presents the breakdown of costs incurred in manufacturing the goods sold during the year. This is computed using the:

Cost of Goods Sold Formula = (Cost of Raw Materials Available for Manufacturing + Direct Costs + Finished Goods Inventory, Beginning) – Finished Goods Inventory, End.

Raw Materials Inventory****, Beginning represents the value of raw materials counted as unused and unprocessed during actual year-end inventory of the preceding period.

Raw Materials In-Process, Beginning – This is the value of raw materials that went into production but were inventoried as still in process at year-end date of the preceding period.

Raw Materials Purchases - The value of additional raw materials purchased during the year.

Cost of Raw Materials Available Formula = Raw Materials, Beg. + Raw Materials In-Process, Beg + Raw Materials Purchases

Raw Materials, Inventory Ending - The value of the raw materials actually counted as still on hand and unused as of year-end inventory for the current year.

Raw Materials In-Process, Ending - This is the value of raw materials that went into production but were inventoried as still in process of production as of year-end closing for the current year.

Cost of Raw Materials Used - The value of the total raw materials used actually converted into raw materials into finished goods.

Cost of Raw Materials Used Formula - Cost of Raw Materials Available for Manufacturing – (Cost of Raw Materials Inventory, Ending + Cost of Raw Materials In-Process, Ending)

Direct Labor Costs - This represents the salaries paid to all company personnel who had a direct hand in the manufacturing process of the Cost of Raw Materials Available for Manufacture.

Direct Utility Costs - The cost of electricity, water and communication facilities used in the plant area or where the raw materials were produced and completed as Finished Goods.

Direct Overhead Costs are the indirect labor, indirect materials and supplies as well as other indirect expenses, in the sense that they may not be directly related in the manufacture of the goods sold but the nature of the expenses’ incurred was directly related to the manufacturing process.

Cost of Goods Manufactured and Available for Sale – Represents the total costs of producing the goods that were completed and added to the finished goods available for sale during the year.

Cost of Goods Manufactured and Available for Sale Formula – Cost of Raw Materials Used + Direct Costs

Finished Goods Inventory, Beginning – Represents the goods manufactured and completed from preceding year’s manufacturing process but were inventoried as still on hand and unsold during the preceding year’s closing inventory. They had been added as additional goods available for sale for the current year.

Finished Goods Inventory****, Ending – This is the value of the current year’s ending inventory of goods manufactured for selling activities, but were accounted for as unsold inventory at year-end.

Gross Profit - In this multiple-step Income Statement, the gross profit is computed by deducting the Cost of Finished Goods Sold from the Net Sales.

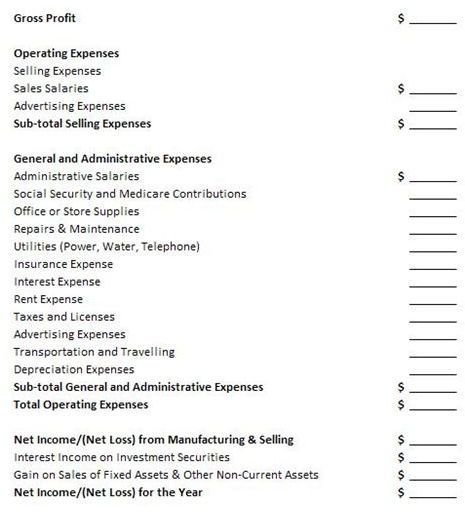

The Net Income after Operating Expenses Section - The image on your right is an example of the Net Income after Operating Expenses of an Income Statement presented in Multiple-Step format.

In a Multiple-Step Income Statement, operating expenses will be sectionalized into selling-related expenses and office-related expenses. This is to readily identify which of the operating expenses can be attributed to the selling activities performed to dispose of the goods manufactured. Such activities are aimed at converting the manufactured goods into revenues.

The Operating Expenses and its breakdown, the Net Income (Net Loss), the Interest Income and the Gain on Sales of Fixed Assets, will all follow the same guidelines provided for the operating expenses in the Single-Step Income Statement. (Please refer to the article entitled Income Statements: Free Template and Example).

As a note, formulas are included in the guidelines, in order to arrive at the sub-totals found under the Gross Profit Section and Net Income after Operating Expenses section, as segmented examples of Multiple-Step Income Statement.

Reference Materials and Images Credit Section

Reference Materials:

- Create a Profit & Loss Statement — https://www.va-interactive.com/inbusiness/editorial/finance/intemp/income.html

- Income Statement — https://en.citizendium.org/wiki/Income_statement#Income_Taxes

Images Credit:

- Sample Images of Gross Profit Section and Net Income after Operating Expenses Section were created for this article by author CS Cantoria.