These examples are best illustrated as year end worksheets, to show transitions from an unadjusted trial balance to an adjusted trial balance.

Objectives

In providing examples of post-adjusted and post-closing trial balances, it is important that we should be clear about the objectives of these trial balances. We will present an organized list of the general ledger accounts which we originally prepared as an unadjusted trial balance worksheet in our article entitled Sample of Unadjusted Trial Balance Worksheet . Once the total debits and total credits of the general ledger account balances have been proven as equal, we are now ready to transform the unadjusted trial balance to its adjusted form.

It should be clear that the adjusting entries referred to here are mostly for valuation purposes in order to recognize the actual income earned during the year, to be matched with the actual expenses related to said income. Valuation will also include estimates in the depreciable costs of assets. In addition, it may also include adjusting entries for errors arising from incorrect accounting entries or entries that were overlooked and un-posted during the year’s entire accounting cycle. Our main guide will be the list of general ledger accounts contained in the unadjusted trial balance worksheet.

Once we arrive at the proper values of the general ledger account balances, we will then proceed with the closing entries. In order to have a full understanding of the closing entries, it is important that the reader knows which general ledger accounts will be closed or zeroed out in their respective general ledger pages. For this purpose, an understanding of the difference between real accounts and nominal accounts will help the reader determine which accounts will be closed.

Below are separate explanations about the steps involved in preparing year end worksheets that contain post adjusting entries and post closing entries to transform one type of trial balance into another.

Example of Year End Worksheet for Post Adjusted Trial Balance

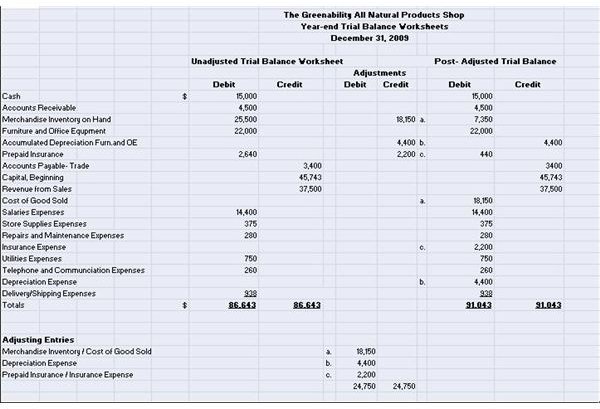

An example of a year end worksheet will present the transition of the sample unadjusted trial balance into its post-adjusted form. Please click on the image on your left and you will see in a larger image view that the standard year end adjusting entries were incorporated in the worksheet. Through the use of this year end worksheet format, you can arrive at the proper valuation of the general ledger accounts affected by accruals, deferments, estimation and physical inventories. There is a downloadable image of this year end worksheet, available at Bright Hub’s Media Gallery -Example of Year End Worksheet for Post-Adjusted Trial Balance. Please find below the explanations for each adjusting entry.

Adjusting Entries to Arrive at the Post-Adjusted Trial Balance

Using the Sample Unadjusted Trial Balance Worksheet provided in a related article with the same title, we will pass adjusting entries to transform said trial balance into its adjusted state. Based on the accounts listed therein, the following accounts will be adjusted based on specific conditions that were present at year end.

a. Merchandise Inventory- Based on actual physical inventory of the stocks which remained unsold at year end, it had an overall residual value of $ 7,350. This means that most of the Merchandise Inventory on Hand amounting to $25,500 held at the beginning of the year was sold during the year’s business operation.

- It is important therefore that the actual inventory value be recognized as the Merchandise Inventory on Hand at year end.

- The difference between the inventory beginning and the inventory at year end of $ 18,150 now represents the cost of goods sold during the year.

- The related adjusting entry for the closing inventory will be:

Dr. Cost of Goods Sold_________ $18,150

Cr. Merchandise Inventory on Hand_________ $ 18,150

In making this entry, you will note that the post-adjusted trial balance will now reflect the actual amount of Merchandise Inventory on Hand while the Cost of Goods Sold has been added as a new general ledger account.

Please proceed to the next page for a continuation of the adjusting entries to arrive at the post-adjusted trial balance.

Adjusting Entries to Arrive at the Post-Adjusted Trial Balance (continued)

b. Furniture and Office Equipment- Part of the accounting cycle is to provide for estimates for valuation and these include the depreciated costs of fixed-assets used in the business operations. Instead of recognizing as expenses the acquisition costs of these assets at the time of purchase, annual depreciation expenses based on allowable and GAAP recognized estimated rates are used to compute for the depreciation expenses. Given that the entire depreciation costs of the fixed assets for the year is $4,400, our adjusting entry will be:

Dr. Depreciation Expense- Furniture and Office Equipment _________ $ 4,400

Cr. Accumulated Depreciation- Furniture and Office Equipment __________$ 4,400

- This entry created two additional accounts; one of which is the Accumulated Depreciation, classified as a contra-asset account to provide a ready estimate for the net book value of the Furniture and Office Equipment. The other is the Depreciation expenses account since the fixed assets were depreciated while in use during the course of the business operation.

c. Prepaid Insurance- This is an example of an account where the accrual method deferred the recognition of the expense at year end while the remaining balance of the prepaid account will be deferred for next year’s accounting cycle. Given that insurance expense was prepaid up to Feb, 28 2011 and that the total insurance premium applicable for the year is $2,200 the prepaid insurance account will be left with a balance of $ 440 representing the amount of prepayment for January and February 2011. The following adjusting entry will be made:

Dr. Insurance expense _________$ 2,200

Cr. Prepaid Insurance _________$ 2,200

Based on these examples of year-end adjusting entries, we were able to come up with an Example of Post Adjusted Trial Balance.

The next page presents the post-closing entries to come up with post-adjusted trail balances as a prelude to financial statement preparation.

Example of Year End Worksheet for Post-Closing Trial Balance

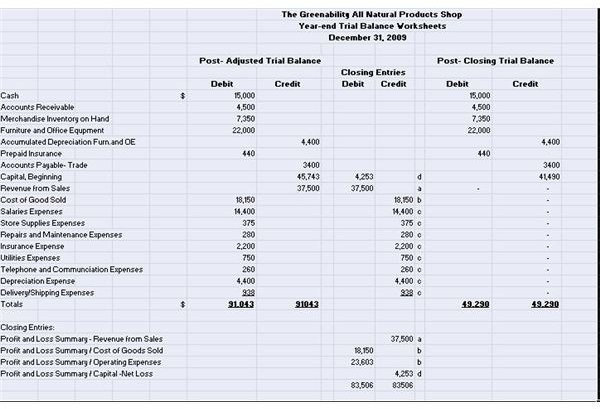

We will continue with the example post adjusted trial balance by using the said adjusted balances as bases for the post-closing entries.

The image on your left is an example of a year end worksheet for post-closing trial balance which you can also view at Bright Hub’s Media Gallery- Example of Year End Worksheet for Post-Closing Trial Balance .

Kindly click on the image to have a larger view, so you can take note that not all general ledger accounts will be zeroed out of their balances via year-end closing entries. Only the accounts included in the Income Statement will be affected which is a process necessary to arrive at the Net Income for the year.

As added information, accounts used for Income Statement reports are called nominal accounts and are used for the purpose of naming and classifying the business’s related income and expenses. They will be closed against the Profit and Loss Summary to determine the Net Income. Once the net income is established, the real account it will lead to is the Capital Account for single proprietorships and Retained Earnings for corporations.

A real account is one that carries a balance that will be forwarded to the succeeding year’s general ledger books; hence, they are not subject to closing entries. These real accounts are presented in the Balance Sheet report and the balances reflected are as of a given period and not for a particular accounting cycle.

Examples of Post-Closing Entries Based on the Post-Adjusted Trial Balance

Based on the above-explanation and the final amounts of the example of post-adjusted trial balance we came up with earlier, the following closing entries will be posted in order to zero-out the balances of these nominal accounts in the general ledger:

You may want to click-on the image on your right to view a screen-shot image on how the general ledger page for the profit and loss account will look like.

Post Closing Entries:

a. Dr. Revenue from Sales _________$ 37,500

Cr. Profit and Loss Summary ________$ 37,500

b. Dr. Profit and Loss Summary __________$ 18,150

Cr. Cost of Goods Sold __________$18,150

c. Dr. Profit and Loss Summary________ $23,603

Cr. Salaries Expenses________$ 14, 400

Cr. Store Supplies Expenses________ $ 375

Cr. Repairs and Maintenance________$ 280

Cr. Depreciation Expenses________$ 4,400

Cr. Insurance Expense________$ 2,200

Cr. Utilities Expenses________$ 750

Cr. Tel. & Com. Expenses________$ 260

Cr. Delivery / Shipping Expenses________$ 938

d. Dr. Capital Account - Net Loss________$ 4,253

Cr. Profit and Loss ________$ 4,253

Note that after the closing entries were posted, the post-closing trial balance revealed the final general ledger accounts and their balances, which will be carried forward to the succeeding year’s books of accounts, . Once this has been achieved, the final stage of the accounting cycle which is the preparation of the year end financial statements will be the next task at hand.

As a summary, the explanations and examples show the transition of post-adjusted trial balance from its unadjusted state and subsequently to its final transformation as a post-closing trial balance.These are the methodical and organized accounting procedures used to ensure that the financial statement reports reflect the most accurate and balanced summary upon closing of the general ledger books at the end of the accounting cycle.

Reference:

The explanations and examples of post adjusted and post-closing trial balances were created by the author for this article.