The Basics of Cash Flow Estimation: Evaluating Profitability Vs. Risks

Differentiating Between Budget and Investment Estimates

In discussing the fundamentals of determining the expected net cash increment of a project, it is our objective to arrive at an understanding of its use as a tool for evaluating the feasibility of a venture. This is in light of contentions that many undertakings have failed as a result of poor estimations.

However, the first step is to eliminate the confusion between cash flows developed for budgetary and for investment purposes.

Budget Estimates

Budget projections for all the incoming and outgoing cash of the business will enable the organization to run its operations under a controlled system of appropriating the working capital fund. The main goal is to ensure that at the least a reasonable amount of profit will be generated from the actual cash collected after all cash expenditures incurred in the same period have been deducted.

Understand that the working capital fund is for defraying the cost of operating the business in order to generate profit. The normal expectation is to recover the portion of working capital used during the business cycle from the cash generated in the same period. Thus the estimations developed in the budget are boundaries by which all costs are controlled to ensure that its total will not exceed the forecasted cash inflows. This is to make certain that profits and not losses will be realized at the end of the business cycle.

Hence, a successful implementation of the budget will result not only in the realization of profits but also in the recovery of the working capital that was used.

Investment Projections

Estimating the cash flow of a project comes as a separate calculation from the budget projections. The latter serves as the baseline for the incremental effect of a venture on the cash position of the business entity. This denotes that the projected cash inflows and cash outflows of the project are not at all related to the ordinary course of the business operations.

Henceforth, if the venture is accepted or assumes an “all-systems-go status”, the normal expectation is that the net cash flow (inflow less outflow) of a completed venture will increase the budgeted net cash flow that will be added to the financial resources of the business.

Basic Principles to Observe

Forecasting the inflows and outflows of a venture requires the observance of certain principles in developing a set of cash projections. They serve as guidelines for determining the relevant or irrelevant items to be included or discounted in order to come up with the best cash flow estimation (CFE).

The most vital of these principles are (1) consistency (2) incremental and (3) separation.

(1) Consistency Principle

This principle takes into consideration two important aspects that can affect or be affected by the quality of the estimations: the investors’ expected income and inflation.

The project manager should bear in mind that some investors provide capital funds for the project usually in the form of bonds. They are contributing funds with the expectation that the bond instrument will yield profits in the form of interests. However, the rate of return should be consistently calculated as the net of all costs incurred to sustain the project. Thus, before presenting the viability of the project to investors, offers of potential rates of return should be net of the project’s estimated costs, including taxes.

In addition, the principle of consistency should likewise be applied when taking into account the occurrence of inflation. Consistency here means if an inflation rate will be applied to increase the investor’s expected income, the inflated costs incurred in generating the income should likewise be considered. Any interest paid as the cost of borrowed capital funds should also be calculated by using inflated interest rates.

If the CFE does not take into account the occurrence of inflation but instead makes use of real cash flows, then real interest rates should be used to increase the value of expected income and to increase the value of anticipated costs.

(2) Incremental Principle

All projects are being considered in terms of their potential capability to increase the profit or improve the present financial condition of a business. Hence, most decisions are initially evaluated based on the proposed project’s potentials to generate additional net cash inflow. There are three factors to consider: (1) the side-effects or “externalities”, (2) the sunk costs and 3) the opportunity costs.

Side Effects or Externalities

If a new venture, let’s say a new product line, is expected to increase the sales of another product, the projected increase related to the other product should be included as part of the cash flow estimation. In similar manner, if the opposite is expected to happen, in which the sales of still another product will decrease because of the new venture, the estimated decrease shall be included in determining the projected cash out flow of the new venture.

Possible increases or decreases that will affect other business aspects, in the event that the new venture becomes an integral part of the organization, are referred to as the side-effects or the externalities.

Sunk Costs

This type of cost is quite complicated and has frequently been mistaken as one that is of critical value in CFEs, but that should not be the case. Sunk costs are regarded as unrecoverable costs that the business has to incur as an expense regardless of whether the new business venture produces incremental yields or not. Oil and gas companies, for example, incur substantial amounts of expenditures that are regarded as sunk costs.

If an oil-exploration project is successful, bond investors who provided the capital fund for the project can expect a high rate of return. The sunk costs incurred for the preliminary drilling expenses as the means to discover the oil-well will not cause any reduction in their expected yields. If the exploration does not produce any viable sources of income, their investments remain intact since they are recognized as liabilities of the organization.

Yet as far as the accounting system and determination of profits are concerned, these sunk costs are part of operational expenses. Thus, they tend to affect the actual cash position of the business if it is a stand-alone project, much to the detriment of the regular shareholders. This is one reason why some major shareholders tend to vote for the continuation of near-dead projects; their decisions are based on the hopes that part of their cash infusion can still be recovered once the venture comes into life as a profit-yielding investment.

If a project uses idle funds that could have earned a considerable amount of interest had they remained as business funds maintained in the form of investment placements, then the amount that should have been earned forms part of the CFE. Foregoing the interest yield reduces the cash inflow of the business and therefore, should be regarded as part of the costs incurred by the business once the approved project goes underway.

(3) Separation Principle

In establishing the difference between budget and investment estimates, knowledge has been imparted that the cash inflows and cash outflows of a new venture are segregated from the regular business operations. This is to ascertain, whether or not, the resulting net cash flow of the project will positively or negatively impact the present earning capacity of the business.

Comprehend from the previous discussion of how certain financing costs have tendencies to impact the actual cash position. Said costs are pitted against incremental effects that are based only on projections; hence, the actual costs are creating burdens on the cash position of the company, while the project is currently on-going. This now introduces the element of risks due to the uncertainty of the project’s actual profitability.

Summarizing the Purpose of CFE as a Tool for Gauging Profitability

In understanding the purpose for which a project’s net cash flow is evaluated, it can be surmised that the measure of profitability arrived at, denotes the value of the risks being undertaken by the organization and its shareholders.

The results of the evaluation will determine the project’s burden on the resources of the business if a proposition is accepted. A comprehensive estimation of cash flow enables management to visualize how the new venture will impact its present financial resources, its current operations and if the expected outcome is worth the risks to be taken.

References

- Principles Of Cash Flow Estimation -http://finance.mapsofworld.com/corporate-finance/cash-flows/principles-estimation.html

- Image: INFALTION the method of measuring inflation rates by HWPO (Hard Work Pays Off) under Free Art License

- Project Cash Flow Estimation Financial Management —- http://webcache.googleusercontent.com/search?q=cache:Lp6ZDLQOgokJ:faculty.philau.edu/malhotrad/642Cash%2520Flow%2520Estimation.ppt+what+is+cash+flow+estimation&hl=en&gl=ph

- Cash Flow Estimation and Risk Analysis — http://webcache.googleusercontent.com/search?q=cache:Y3tiHnpZ59cJ:www.willamette.edu/~fthompso/501/Fin11.pdf+basics+of+cash+flow+estimation&hl=en&gl=ph

- Image: Pillars of the failed w:Bangkok Elevated Road and Train System (BERTS) project by Ron Morris under CC BY SA 3.0

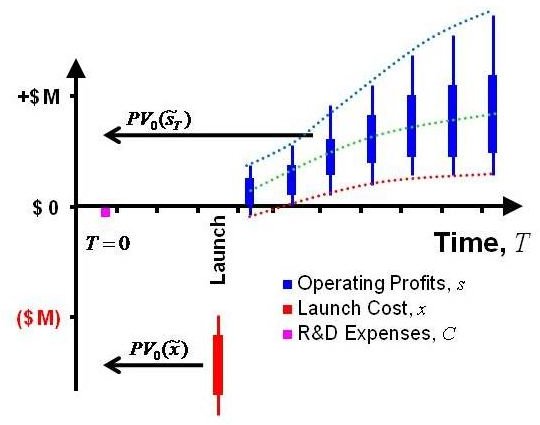

- Image: Typical Project Cash Flow with Uncertainty by Scott Mathews under CC BY SA 3

- Image: Types of offshore oil and gas structures by NOAA Office of Ocean Exploration and Research National Oceanic and Atmospheric Administration under public domain

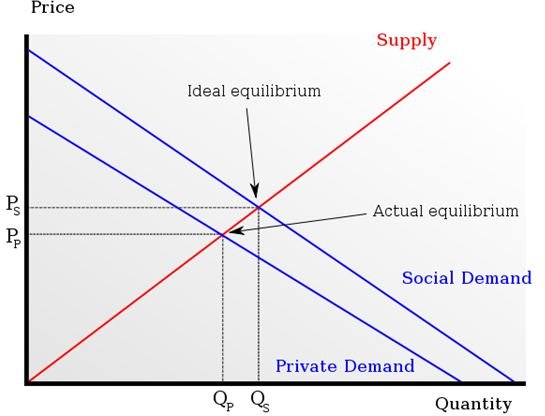

- Image: A supply curve diagram illustrating the microeconomic concept of positive externality by Struthious Bandersnatch under CC0 1.0 Universal

- Image: United States gross federal annual spending from 1901 to 2006 by 84user under public domain