Tips on Learning the Difference Between Accounts Payable and Notes Payable

Defining Payables

Creditors and investors need to look at a company’s liquidity. A company with high levels of current liabilities or weak liquidity could possibly be deficient in financial flexibility. Current liabilities refer to short-term obligations or debts a company must pay from its current assets within a year or less. So what is the difference between accounts payable and notes payable, which are two important elements found on the balance sheet under the heading Current Liabilities section? Here you will learn how to distinguish each of them.

Payables: The Accounts

Accounts Payable (AP) are the amounts a company must pay its creditors in response to the purchase of goods and services. Written agreements such as invoices can possibly support these transactions.

As an example, on February 18, 2011 your company purchases office supplies of $500 and asks for an immediate delivery. The products come the next day and you receive a delivery receipt. On February 23, 2011 the supplier sends an invoice out to your company, saying that the payment for those office supplies will be due within 30 days. Consequently, your company makes a general journal by debiting Office Supplies Expense and crediting AP. With that said, APs are due between the time of receipt of either goods or service, and the payment process for them.

Payables: The Notes

Notes Payable (NP) are specific written promises to pay obligations or debts indicated as short term or long term to banks or loan companies depending on the due date. These notes occur because of purchases, cash loans, and financing.

The company can possibly borrow a certain amount of money from bank or a loan company. In return, the company promises to pay interest periodically and pay the principal when the note is at its maturity date. For example, your company borrows $500,000 from a bank on January 1, 2010 for a year at annual interest rate of 12%. The company would record the cash received in the general journal on January 1, 2010 by debiting Cash and crediting NP of $500,000.

If the company uses the monthly accounting period, then every month it needs an adjusting journal entry to record Interest Expense and Interest Payable of $5,000 ($500,000 x 12% x 1/12).

Likewise, when your company applies the annual accounting period, it needs an adjusting journal entry on December 31 of $60,000 ($500,000 x 12% x 12/12).

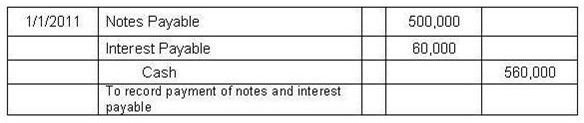

On January 1, 2011 your company has to pay the principal amounting to $500,000 and $60,000 interest ($500,000 x 12% x 12/12) when it comes to the maturity date. Therefore, NP of $500,000 and Interest Payable of $60,000 are debited in a general journal, while Cash of $560,000 is credited.

The basic distinction between both current liabilities is notes payables impose interest rates, which have a specific maturity date. In addition, NPs also emphasize the company borrowing money must pay the principal at maturity, while accounts payables do not have this requirement.

References

Kieso, Donald E., Weygandt, Jerry J., & Warfield, Terry D. Intermediate Accounting, 12th Edition. John Wiley & Sons, Inc. (2007, December)

Interest-Bearing Notes: Current Liabilities - https://www.financial-accounting.us/fa/8/interest-bearing-notes.php

Screenshots courtesy of author