How To Interpret Cash Flow Statements

Interpreting Cash Flow Statements

Cash flow statements provide valuable information about a firm’s financial performance, but knowing how to interpret cash flow statements takes some understanding. Cash flow statements are used as an analytical tool to assess the ability of a firm to cover its operating costs in the short-term and assist in the evaluation of a firm’s value.

Analyzing the Cash Flow Statement

The cash flow statement comprises of three main segments:

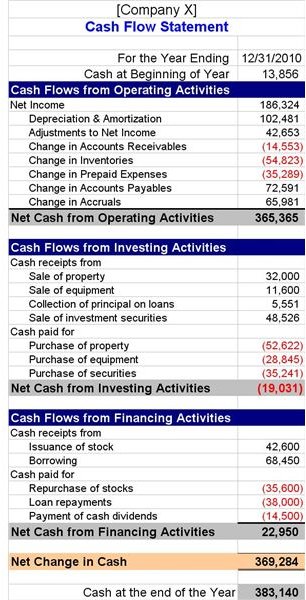

1. Cash flow from Operating Activities

This segment summarizes cash inflows and outflows associated to the firm’s fundamental operations. Cash flow from operating activities is calculated by adjusting net income to mirror changes in depreciation & amortization, accounts receivable, inventory, prepaid expenses, accounts payable and accruals. Increases in accounts receivable, inventory and prepaid expenses are subtracted from net income while decreases are added. Decreases in accounts payable and accruals are subtracted from net income while increases are added.

**

2. Cash Flow from Investing Activities

This segment summarizes cash inflows and outflows associated to the purchase and sales of non-current assets. Such activities may include the firm’s property, plant and equipment, sales of investment securities and collection of principal on loans.

3. Cash Flow from Financing Activities

This segment includes activities associated to the firm’s debt and equity financing. Such activities may consist of issuance of stocks or equity, stock repurchase, borrowing, loan repayments and dividend payments.

The net increase or decrease in the firm’s cash flow is calculated by adding the net cash flows from operating, investing and financing activities.

Why Cash Flow Statement is Important to Investors

The cash flow statement helps investors, but also a firm’s stakeholders, to make well-educated decisions on future investments. By summarizing the cash inflows and outflows, the cash flow statement not only reflects a firm’s financial solvency, but it also allows executives and investors to compare the firm’s current financial standing with past periods, and helps to determine whether its net cash flows have increased or decreased.

Although the cash flow statement is very important in determining a firm’s financial health, the income statement also provides valuable information that can assist investors in deciding if a firm is of good value. However, even if a firm has negative cash flow on a given quarter, it may generate positive cash flow from its operating activities over the next quarters and have positive overall cash flow at the end of the fiscal year. Positive cash flow is an optimistic indication, but negative cash flow is not necessarily a bad sign, because it may not reflect the firm’s potential in all business sectors.

Important Tips When Interpreting a Cash Flow Statement

Some important tips that can help investors interpret cash flow statements to evaluate a firm’s financial health include:

-

The cash flow statement summarizes the cash inflows and outflows of the firm. If a firm has consistently more inflows than outflows, it is an indication that it can increase its dividend payments, repurchase its stocks (share buyback), reduce its debt or acquire another firm. All these are signs of a firm that is in good standing and is considered to be of good value.

-

The cash flow from operating activities should always be positive and greater than zero. This indicates that the firm has strong potential for growth. However, investors should be wary of any growing gap between the firm’s reported earnings and the operating cash flow. If the firm consistently reports growth on its income statement, but has negative cash flow, it may be lacking the ability to translate its growth into cash. These firms are more likely to face liquidity problems, or even default on their short term liabilities. If the firm consistently reports operating cash flow that is greater than its net income, it may be gaining momentum in revenues.

-

The cash flow from investing activities indicates a firm’s ability to invest in non-current assets. If the company generates enough cash to invest continually in property, plant and equipment as well as other fixed assets, it is an indication that the firm aims at replacing technologically obsolete equipment to keep up with the latest trends.

-

The cash flow from financing activities should be carefully evaluated when interpreting cash flow statements. Investors should compare current debt financing with past periods to determine if the firm has reduced its debt over the years.

Conclusively, the cash flow statement is a useful analytical tool to assess a firm’s financial health if one knows how to interpret cash flow statements correctly. Typically, if a firm is consistently generating more cash than is using, that firm is considered to be of good financial standing and value. However, the cash flow statement should be analyzed in comparison to the balance sheet and the income statement, to assist investors in evaluating the firm’s future growth potential, and to help executives in determining if the cash generated is sufficient to fund the firm’s short term liabilities.

Resources

Cash flow from operating activities - https://www.investopedia.com/terms/o/operatingcashflow.asp

Cash flow from investing activities - https://www.investopedia.com/terms/c/cashflowfinvestingactivities.asp

Cash flow from financing activities - https://www.investopedia.com/terms/c/cashflowfromfinancing.asp

Image Credit: - Cash Flow Statement created for this article by author Christina Pomoni

This post is part of the series: Financial Statement Analysis

Financial statement analysis (FSA) helps managers predict future earnings, dividends and free cash flow. Analysts use FSA to derive information about the relationships between individual values in the financial statements and identify problem areas and opportunities within a firm.