How to Determine Accounting: Customer Loyalty Programs

What Is a Customer Loyalty Program?

As an automotive dealer, I often give away a free lube-oil-filter service if someone purchases something such as a car, a more expensive service, parts, or accessories. Credit card, hotel, and airline companies that give away points for shopping or flying are also examples of customer loyalty programs.

So, what are the rules for accounting customer loyalty programs? Well, there is the old-fashioned way and then there are the guidelines implemented in 2007 by the International Financial Reporting Issues Committee (IFRIC) that most follow these days when it comes to customer loyalty programs.

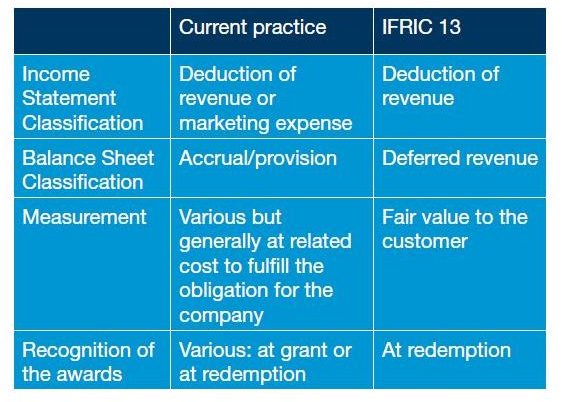

The screenshot to the above-left (click to enlarge) shows the old and the new ways on accounting procedures for customer loyalty programs and what financial documents they affect. As far as CPAs are concerned, however, either procedure is fine as far as following IRS guidelines. A good read on proper accounting procedures, especially when it comes to determining a customer loyalty program, is offered by the IRS. Another great publication for determining what qualifies as a customer loyalty program is the one offered by Price Waterhouse Cooper (PWC).

Screenshot by author courtesy of PWC

On to the Accounting Procedures

Once you’ve clarified you indeed are offering customer loyalty programs, you need to consider a couple things:

- Delivery – when will the reward be redeemed?

- Revenue – did you receive revenue in return for offering the reward?

If you answer yes to either of these questions, you need to determine what general ledger accounts will be affected—what entries are necessary as far as debits and credits and to which accounts.

Examples of Debits and Credits

For our example, let’s say I own an airline and offered my loyal customers 100 flying points toward their account each time they fly with my airline. My rules and guidelines for points say they never, ever expire and can be carried from year to year.

I must consider this revenue because I require my loyal, loyal customers to fly before they are rewarded with any points at all—meaning they bought a ticket! Let’s take a look at how I would debit and credit general ledger accounts:

- Debit -- Reward Program Expense – $100

- Credit – Sales Customer Loyalty Revenues - $100

But hold on! What if my loyal, loyal customers only use 50 of those offered points in the first year?

- Debit – Reward Program Expense - $100

- Credit – Sales Customer Loyalty Revenues - $50

- Credit – Deferred Customer Loyalty Revenues - $50

Once the loyal, loyal customer uses the remaining 50 points, I simply:

- Credit – Deferred Customer Loyalty Revenues - $50

- Debit – Sales Customer Loyalty Revenues - $50 – this clears out the entry.

While this example is a very simple example, the best way to determine your accounting for customer loyalty programs correctly is to talk with your in-house controller or bookkeeper or ask your tax professional. The publication from PWC (link above) is also very helpful in offering debit and credit designations to the appropriate accounts.

Image Credit (FreeDigitalPhotos)

Affected Financial Statements

When looking at various customer loyalty programs, some financial documents will be affected. For example, the income statement will show a deduction in revenue; the balance sheet will show deferred revenue.

Finally, keep in mind that some offerings are not considered customer loyalty programs. For example, if you offer coupons to customers that walk into your establishment, but don’t require them to buy anything, this is not considered a customer loyalty program. If you offer a discount coupon attached to a product or service a customer must purchase before they receive the discount, then that is considered a customer loyalty program. If you’re unsure how your offerings are looked at per accounting guidelines, ask your tax professional.