Understanding Accounting Source Documents - Their Basic Characteristics and Control Features

What are Accounting Source Documents?

Accounting source documents are the primary reference materials used as the bases for the basic acts of recording and summarizing business transactions. Each organization or entity may have distinct features and structures of business forms that are readily identifiable as documents that originate from their end. However, accounting standards require that these business forms contain information that are basic for recording purposes.

What are the Basic Characteristics of Accounting Documents?

As reference material for accounting purposes, they should possess the following basic characteristics, but should not be limited to:

-

Information pertaining to date, amount, nature or explanation of transaction, and the name of the issuer. Some other data or control features may be required and depend on the type of transaction for which purpose the accounting source document was accomplished.

-

Traceability; it is important to include information, usually reference codes, that will link one accounting source document to another as they flow from one accounting process to the next and from period to period. That way, errors if any can be pinpointed while the audit examination is provided with audit trails.

-

A single type of document should have more than one copy, in accordance with the double-entry system of bookkeeping. In fact the more users involved as parties to a transaction, the more copies should be available. In addition, all copies should contain concise, consistent, and legible information.

-

Source documents may be manually written or encoded or electronically generated. However, certain regulations require the addition of certain features that would render them legal documents.

-

Some source documents contain number sequencing, pre-numbered as a control feature, and are called accountable forms. Still, not all source documents used for accounting purposes are pre-numbered or qualify as accountable forms.

A closer look at ten of the most common accounting source documents will present readers with a clearer perception about the aforementioned characteristics:

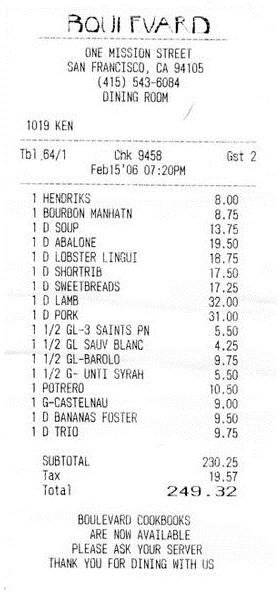

1. Official Receipts –

This document is issued in exchange for monies received and as proof that payment was received or that a monetary condition to pursue a transaction was fulfilled. They may be manually issued or electronically produced forms. However, aside from the basic information furnished by this document, the following features should be indicated in order to qualify the document as a legally recognized “official receipt”:

- It contains the Taxpayer Identification Number (TIN) of the issuer.

- The machine that produced the receipt or tape has been registered with the tax regulatory body that regulates the operations of the business.

- Official receipts, to be legal, have been printed by a registered printer, who will indicate in the printed form his license or printer’s authorization number.

Inasmuch as cash receipts are used for taxation purposes, it is important that these accounting source documents contain features required by the tax regulating body as acceptable proof of payment.

2. Sales Invoices -

Sales invoices are different from official receipts because they merely acknowledge a sales transaction and not the receipt of payment.

Nevertheless, certain transactions may result in business disputes in the future, where the sales invoice becomes necessary as proof or evidence. Hence, the sales invoices should likewise posses the same features found in official receipts in order to be considered as legal.

The manner as well as the terms and conditions of payment for the goods are indicated in this document, whether COD or credit terms.

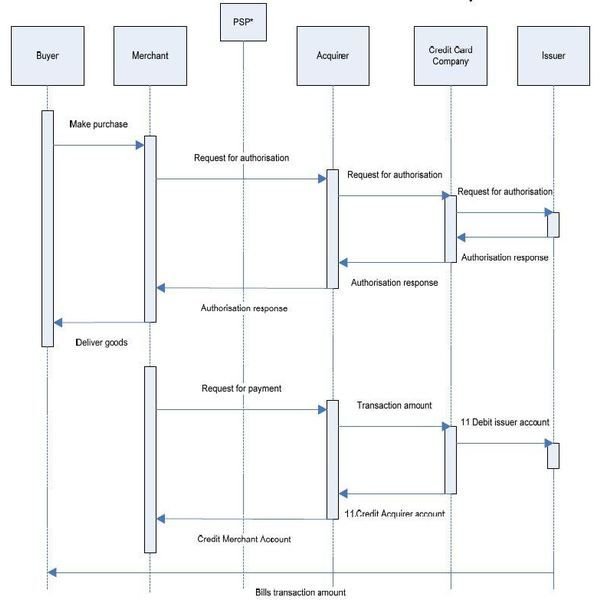

3. Credit Card Receipts -

A credit card receipt is issued aside from the cash receipt generated by the cash register.

This will be the credit card issuer’s basis for reimbursing the business establishment from where the cardholder purchased the goods or services on credit.

Monthly credit card statements will also be supported with copies of these receipts, as supporting documents to the billing statement entries. This type of receipt should also be legally produced in accordance with the tax regulations.

Find more examples and brief overviews about accounting source documents on the next page.

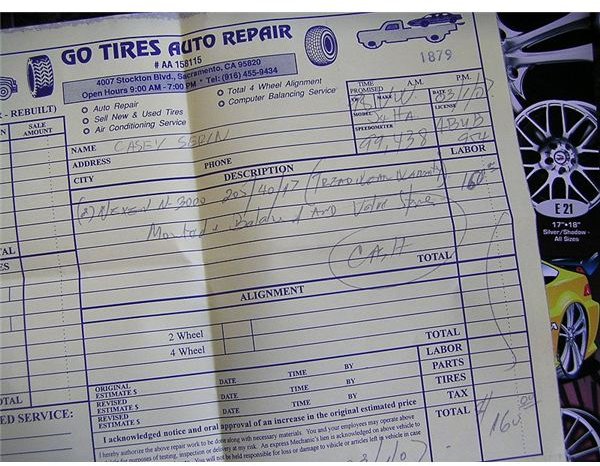

4. Purchase Orders

In a corporate environment, all acquisition and procurements for tangible or intangible goods will form part of the company’s assets, whether for reselling purposes or as implements of the business. They should therefore be supported by a duly approved and pre-numbered purchase order form.

This is to ensure that all major purchases are authorized and within the recognized budget.

However, less than the minimum amounts of purchases or certain cases of emergency shall exempt the procurement from the issuance of purchase orders but all in accordance with the company’s policies.

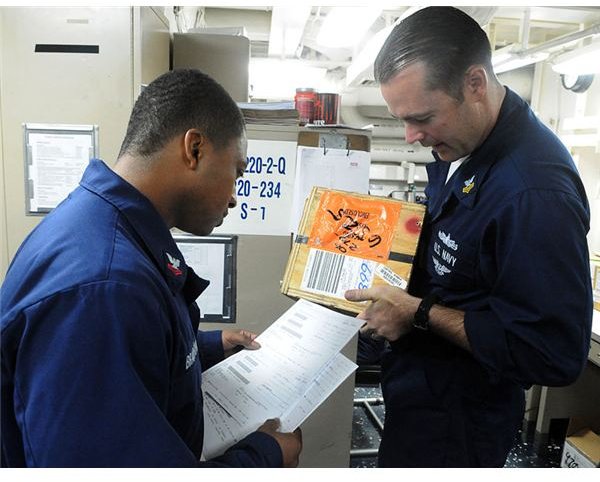

5. Stock Inventory Release / Issuance Form

These forms are essential as proof that only authorized stocks are taken out of the warehouse or storage rooms.

They also form part of the accounting source documents used to reconcile any discrepancy between the stock inventory reports generated by a business machine equipped with the perpetual inventory feature against the actual physical count of the goods on hand.

- Accounting for stock inventory is very important since inventory costs, included and calculated under the Cost of Goods Sold account, are major items considered for determining business performance and profits. Henceforth, all goods coming in or out of the stockroom should be properly documented on a per-item basis.

6. Delivery Receipts

These documents are the counterpart of the stock inventory release forms, as they serve as evidence that goods ordered from a supplier were received intact and complete.

They should be received by an authorized representative of a company, usually in the presence of an internal auditor, to ensure that incomplete deliveries or defective goods are properly reported or returned. Recording of these deliveries should likewise take note of unit prices and terms of payment.

Copies of the delivery receipt should also form part of the supporting documents before any billing payments are prepared.

7. Deposit Slips

Cash, checks, and other cash items recorded as deposits to a bank account are supported with validated deposit slips in order to qualify as accounting source documents. The bank teller’s validation, the bank’s “Received" stamp, and the receiving teller’s identification and initials will make the deposit slip legal as evidence of the deposit transaction.

8. Canceled Checks

These represent the checks issued by the company to serve as payments for authorized transactions whether for internal or external purposes.

Once presented to the bank for payment either as an over-the-counter encashment or as a bank clearinghouse item, the amount on the face of the check shall be debited or deducted against the issuer’s deposit account.

Checks that have been processed and paid become canceled checks that are returned to its issuer, along with the bank statement for the month that the checks were charged against the account.

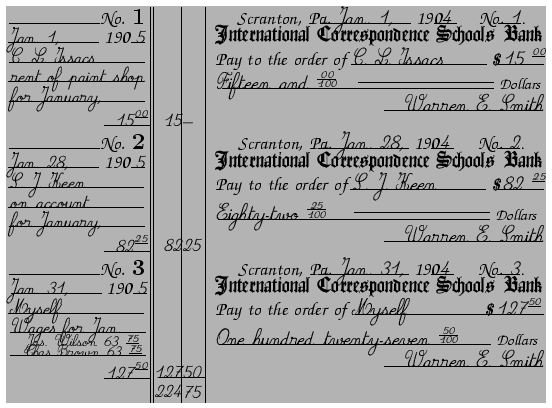

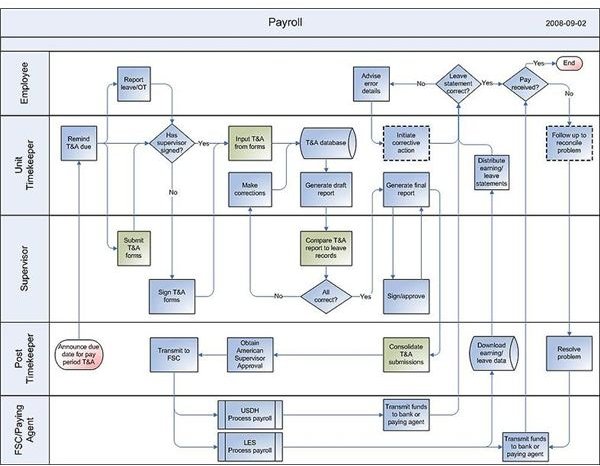

9. Payroll

.

Payroll forms for salaries and wages that are manually paid-out also serve as accounting source documents. They contain the complete details about the total salaries paid, the federal and state taxes withheld, and deductions that form part of the payroll entry.

However, certain information should be supported by the employees’ W4 and Payroll Deductions Authorization forms in order to be considered as a valid basis for accounting entries.

In addition, the signatures of the employees will serve as proof that wages have been paid, as well as a basis for threshing out any complaints pertaining to salaries paid.

10. Promissory Notes

Promissory notes are the best accounting source documents to serve as evidence of obligations or indebtedness. They contain pertinent information about terms, maturity dates, installment payment schedules, amount of debt, and rates of interests and penalty charges.

Inasmuch as several transactions will arise out of these particular transactions, accounting tickets in the form of debit or credit advices are used as accounting source documents for recording purposes. The control officer reviewing and approving the subsequent transactions shall observe it as best practice to check the details of the accounting tickets against the information contained in the promissory note itself.

There are numerous business documents that serve as source documents for accounting purposes, and the ten business forms that have been discussed above are considered as essential for basic, legal, internal control and taxation purposes. Nonetheless, these documents can effectively serve their purposes only if they are properly filed, indexed, and stored.

Reference Materials and Image Credit Section:

Reference: Author cscantoria’s personal accounting files.

Image Credits:

- Official Receipts

- Volkswagen Invoice

- Credit card 20101225

- Network Model.

- [Logistics Specialist 1st Class Todd Tudor conduct an inventory in stock control…](https://commons.wikimedia.org/wiki/File:US_Navy_101116-N-3666S-079_Logistics_Specialist_ 2nd_Class_Travis_Bradford,_left,_and_Logistics_Specialist_1st_Class_Todd_Tudor.jpg)

- Bookkeeping-Checks

- Payroll Process Map

- ColoradoForeclosureFight