Fraudulent Accounting and Enron Scandal Explained

Enron’s “Invisible Hands”

In the annals of accounting, “Enron scandal” means more than just a tale of accounting manipulations. It surpassed all other accounting frauds, because the need to hide its true financial conditions was not just a matter of hiding losses borne out of failed business projections. In our overviews of the ten major accounting scandals that changed the business world, Enron led the pack of white collar crimes committed out of pure greed.

Many blamed America’s deregulated trading system as the main contributing factor that allowed Enron’s malfeasance to take place. However, a review of the early years of deregulation had proven that free enterprise was not as bad as its detractors had expected.

Accordingly, oil prices fell during the first half of the 1980s and that public anger against trade deregulations abated–so much so that the “Windfall Profits Tax” was repealed by Congress during President Reagan’s administration. It was a tax measure to counter against excessive profiteering and was enacted under President Carter’s administration.

The early years of deregulation supported the views of the great Scottish moral philosopher, Adam Smith. He saw free enterprise as an economic doctrine. In his 1776 publication called “An Inquiry into the Nature and Causes of the Wealth of Nations,” Smith philosophized that an unrestricted market creates an “invisible hand,” where the entrepreneur’s self-interest will guide him into making the most efficient use of his resources. Public welfare and benefits are only by-products of all the efforts exerted to succeed in his quest for profits and business prominence.

In the case of Enron, the “invisible hand” and the matter of self-interest did exist. However, what was lacking was concern for public welfare and benefit, because through the very end, CEO Kenneth Lay exerted efforts to deceive the public and Enron’s employees.

Kenneth Lay sent emails that were supposedly meant to allay employees’ fears regarding rumors that Enron was about to fold. The emails included instructions for employees to hold on to their shares of stocks and should even buy more. A short while after, Lay and other top executives unloaded more than a billion dollars’ worth of stocks wherein Enron’s CEO profited in the amount of $103 million.

The Factors that Contributed to Enron’s Betrayal of Public Trust

Enron actually took advantage of America’s free enterprise—where industries are expected to be motivated into earning profits by providing consumers the best services or commodities they need. Under unrestricted trade conditions, industry players are expected to formulate their own business and financial strategies in ways that will attract consumers to patronize their goods and services.

However, Enron executives became greedy in America’s deregulated economy where business entities were afforded tax cutbacks. Said cutbacks were intended as incentives for businesses to deliver the best quality in their commodities at competitive prices. That way, companies and entrepreneurs alike could generate profits that would give investors encouraging yields on the funds that they contributed .

Yet Enron’s top level executives saw all these as loopholes. Free trade presented opportunities to ensure profits for themselves and for their investors. In the final and true accounting of Enron’s books, the investors actually didn’t gain because the money that was paid out to them as dividends mostly came from borrowed funds and from the capital markets.

Nonetheless, a detailed look at the Enron accounting scandal will reveal that this corporate giant’s misdemeanors would not have been possible, if not for the connivance of other institutions and the failure of federal regulators.

Through all of these, the investing public was complacent that all information supplied to them as bases for their investment decisions was founded on verified facts. Little did they know that they were fictitious data supported by blatant certifications and endorsements.

Proceed to the next page for the continuation of this detailed report about the massive accounting anomalies perpetuated by Enron .

Enron’s Massive Disinformation Campaign

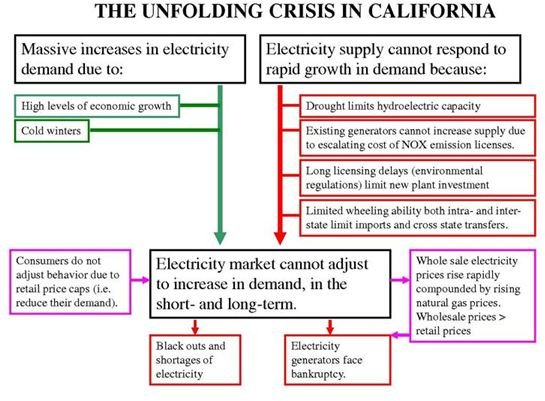

Enron misled the public into believing that it was realizing profits from legitimate trading of its natural gas to energy distributors. In one of the senate investigation hearings, some of Enron’s site employees testified that they were instructed to intentionally withhold or cut off gas supply in California in the year 2000. (Click on the image to view a diagram for a purported analysis of California’s energy crisis).

During the summer of that year, the entire state experienced what were then called “rolling blackouts.” Gas pipelines appeared to be clogged due to heavy demands, but in truth they were intentionally shut down to create artificial gas shortages.

The transition from a highly regulated to a deregulated gas trading industry during the mid-80s made it possible for Enron’s trading techniques to work to their advantage. Wall Street analysts and other stock market observers perceived the seeming scarcity of available gas supply as due to heavy trading. Shorter supply matched against higher demands meant commanding a higher selling price.

Enron’s traders helped in building up the “robust selling” scenario by publishing press releases about trade deals that did not actually take place.

Hence Enron’s 2000 financial reports disclosed revenues of over $100 billion, which made the company the 7th highest revenue earner among America’s largest corporations. In the same year, Enron’s stocks were selling at $90 per unit, which placed Enron’s market value at $700 billion.

Naturally, Enron’s top executives reaped their own rewards. Enron’s CEO, Kenneth Lay, in particular reportedly earned $1.3 million in basic salaries plus $7 million in bonuses and shared profits and exercised stock option rights that earned him $2.3 million.

Even President Bush gained from Enron’s transactions, since the latter reportedly contributed $2 million to the former president’s campaign funds for that year.

However, there was one problem in all scenarios that were set-up: There was no actual money coming in from real revenues but only those that came from investors. All the revenues reported were products of accounting manipulations orchestrated by Enron’s Chief Finance Officer Andrew Fastow. In fact, whatever money that was paid out as dividend to stockholders came from the investors themselves and not from profitable gas and energy trading transactions.

Citigroup Bank’s and JP Morgan Chase’s Participation in the Enron Fraud

In order to solve the company’s cash deficit, Enron had to resort to substantial borrowing that was provided by Citigroup and JP Morgan Chase. Still, it was important for Enron to maintain its credibility as a largely liquid company, in consistency with its image as a high-revenue earner.

The debt-cover-up scheme involved Enron’s establishment of bogus companies called “Mahoria” and “Yosemite” in Cayman Islands, which appeared to be separate and distinct entities. The senate investigating committee was able to come up with emails and documents that provided evidence of JP Morgan Chase’s and Citigroup’s participation.

These two financial institutions provided Enron a total of $8.5 billion in borrowed funds from 1992 to 2001 by way of 26 transactions, channeled to two of Enron’s fake companies, Mahoria and Yosemite. In order to launder the money as legitimate payments for energy trade deals, JP Morgan Chase and Citigroup allowed the bogus companies to open escrow deposits in favor of Enron, all of which were funded by the bank-granted loans.

Enron was able to get hold of the borrowed funds by simply making it appear that substantial amounts of prepayments were received from energy trade contracts with the bogus companies.

This highly complex manipulation enabled Enron to report increased revenues out of lucrative trades and get hold of actual funds without losing its credibility as a highly liquid company. Naturally, the company’s books became more inflated than ever in terms of assets and revenues. Added to that was the high credit score eaned due to their favorable debt-to-equity ratio.

Enron’s CFO Andrew Fastow took care of the accounting aspect by assigning higher values to the long-term energy contract deals. Instead of booking the sales at the fair market value of the energy or gas, profits were instantly booked by assigning trade values at forecasted amounts supplied by financial analysts. Later on, the long-term contracts were assigned values based on what made Enron appear as more profitable than before.

Please turn to page 3 for more on: Enron Scandal: “Andersen Accounting Turns a Blind-Eye”

Andersen Accounting Turns a Blind-Eye to Enron’s Accounting Practices

A chief auditor of Andersen Accounting (AA) named David Duncan, who was assigned to handle AA’s Enron account, turned a blind eye to all these accounting manipulations. Instead, he supported the erring company’s financial statement with audit reports that certified Enron’s financial statements as all in accordance with generally accepted accounting principles.

During the congressional hearings for Enron’s accounting scandal, it was established that Citigroup Bank earned a total of $167 million from the 26 shady deals that allowed Enron to perpetuate the debt cover-ups. JP Morgan Chase did not disclose their earnings but they agreed to a settlement of $400 million; this formed part of the funds raised in order to return some of the investors’ money. Citigroup, on the other hand, paid $80 million as settlement for their participation in Enron’s debt-cover-up fraud. Accordingly, the Citigroup executives were more cooperative during the investigation, in comparison to their JP Morgan Chase counterparts.

More Fake Companies to Cover-up Enron’s Losses

Since Enron’s cash inflows were basically derived from borrowed funds and investors’ money, CFO Andrew Fastow had to unload some of the company’s losses without hurting Enron’s reputation.

CFO Fastow’s scheme was to use more bogus companies as fronts for Enron’s expansion programs. As accounting scandals came, one after another, the use of bogus companies turned out to be prevalent among other corporate giants. These companies were later tagged as SPEs or special purpose entities, which were utilized to absorb fraudulent companies’ losses. In Enron’s case, they were made to appear as part of the company’s risk diversification strategies.

Accordingly, Enron had more than 3,000 separate SPEs, 800 of them located in offshore jurisdictions. Their roles were to receive funds coming from LJM, a partnership created by CFO Fastow as Enron’s equity investor. The SPE would later return the funds infused by LJM for a larger amount, to make it appear that Enron’s investment in the SPE paid off.

To illustrate these risk diversification schemes, one example occurred when Fastow debited $30 million as LJM investments instead of debiting $30 million expenses in Enron’s books. This accounting manipulation not only lessened the company’s distress but it also enhanced Enron’s net worth, since the investment entry increased the energy company’s assets.

After a while, the SPE would return the supposed investment to LJM for a larger amount; let’s say $40 million, to make it appear that Enron’s investments, coursed through LJM, earned $10 million. Thereafter, CFO Fastow made entries in Enron’s books to reflect the return of the $30 million LJM investment plus $10 million in earnings. It did not matter that these were only book entries because as far as Fastow was concerned, they were all fake transactions using fake companies.

In some cases, these companies incurred losses in order to keep Enron’s book balanced. Fastow’s objective was to make it appear that Enron made money from earnest legitimate ventures but at the same time also incurred losses from some of them. Actually, they were all Enron‘s losses disguised and laundered through the SPE companies that CEO Kenneth Lay and CFO Andrew Fastow created.

Continue to Page 3 for more details about the Enron scandal and how the SEC and Wall Street analysts failed to see through the anomalous schemes.

The SEC’s and Wall Street Analysts’ Failure to See Through Enron’s Financial Reports

At the end of the Enron accounting scandal investigations, the SEC and the Wall Street analysts were partly blamed by the congressional hearing committee for their failure to exercise their duties with utmost diligence. Accordingly, had these two sectors compared Enron’s financial reports with other companies or with the industry standards, they could have noted the large disparities.

In January of 1992, which was the beginning of the gas price manipulations, the chief accountant of the SEC granted Enron permission to use mark- to-market accounting for their gas services. The underlying argument for this method was Enron’s inability to furnish a more accurate presentation of their true liquidity by booking their liquid assets using historical costs. Hence, the use of the market’s price forecasts for their natural gas would create a fairer presentation of their financial position

In 1994, the SEC exempted power marketers like Enron from the Public Utility Holding Company Act (PUCHA). The decision was made based on the premise that said companies, which included Enron, did not operate power plants but merely traded electricity contracts. This particular exemption made it possible for Enron to manipulate their natural gas and stock prices by creating a fake energy crisis.

PUCHA’s essence was for the prohibition of utility holding companies from investing the citizen’s “rate payments” in non-electricity industries or in out-of-region power plants — the reason for this was that such investments would not directly contribute to the improvement of the services being provided to the customers.

Add to that the Enron exemption privileges from the securities laws prescribed under the Investment Company Act of 1940 granted by the SEC during the chairmanship of Arthur Levitt in 1997.

Investigating bodies concluded that these privileges allowed Enron to make use of fake companies or SPEs, where Enron buried their million-dollar debts and losses.

Had the SEC reviewed Enron’s financial statements and its contracts with the more than 3,000 SPEs before awarding said exemptions, the fraudulent transactions and accounting manipulations could have been discovered much earlier.

Enron’s Board of Directors was likewise accused of endorsing all these transactions through their Board approvals, without any records of raising any questions. Accordingly, they were asked by CEO Kenneth Lay to sign a waiver of their rights to question the investments placed by CFO Fastow in the fake LJM investment partnership.

Continue on Page 4 for Accounting: Enron Scandal - What Led to the Discovery of the Enron Accounting Scandal?

What Led to the Discovery of Enron’s Accounting Fraud?

It took an unknown hedge-fund manager named Jim Chanos to notice that there was something wrong with Enron’s financial conditions and business activities. In March 2001, Chanos was said to have gathered Enron’s financial statements and began to scrutinize Enron’s business deals. His position paper was carried in a Texas edition of the Wall Street publication for that month.

Jim Chanos likewise tipped off a Fortune reporter, who later came out with a story entitled “Is Enron Overpriced?" The report basically questioned how Enron made all its money despite the seemingly negative factors that could have created adverse impacts on Enron’s financial conditions. Thereafter, Wall Street Journal reporters picked up the story and, soon enough, rumors about Enron’s shady deals began to spread.

The SEC’s formal investigations into the accounting scandals were merely spurred by rumors and news reports and the plummeting of Enron’s shares of stock from its all time high of $90 per share to $36.88 per share. In October of the same year, the SEC began its investigation of Enron’s questionable financial statements by asking the company to restate its financial reports in accordance with the GAAP rules.

In November of 2001, Enron’s shares of stock had dropped to less than a dollar per share. On December 2, 2001, Enron finally admitted bankruptcy by seeking the court’s protection under Chapter 11 of the US Bankruptcy Code.

Continue to the fifth and final page for a brief summary of the Enron scandal investigations and its aftermath.

Andersen Accounting’s Attempt to Obstruct SEC’s Investigations

As SEC investigations were beginning to unfold, Andersen Accounting’s Duncan obstructed investigations into Enron’s case by ordering AA’s Enron auditors to shred all related key documents. AA’s acting CEO and managing partner, Joseph Bernardino, later admitted in court that he knew about the document-shredding despite the illegality of such acts. AA paid $217 million as settlement and a $500,000 fine for their document shredding.

Before the year 2001 ended, 4,000 Enron employees lost their jobs without any separation benefits, not even their 401k retirement funds. Enron’s Chief Finance Officer Andrew Fastow turned state witness in return for a reduced term of imprisonment and the release of his wife Lea, who was imprisoned for tax evasion. However, CEO Kenneth Lay died of a heart attack even before he was able to serve time in prison.

Summary:

The Enron accounting scandal was a complex system of connivance and political clout. To the Enron officials, it was not the invisible hands of a free enterprise that guided their self-interests, because they did not act as competitors in a system where business ethics were revered. Corruption and connivance encouraged Enron’s executives to carry out their manipulative schemes because they were guided by the invisible hand of immorality.

Reference Materials and Image Credit Section:

References:

- Encyclopedia of white-collar & corporate crime: A - I, Volume 1 By Lawrence M. Salinger–https://books.google.com.ph/books?id=0f7yTNb_V3QC&pg=PA279&lpg=PA279&dq=what+were+the+economic+crimes+of+enron&source=bl&ots=OeQuSR6KWW&sig=w68P4l7Tt61lup97y1yYbjUsvfQ&hl=en&ei=STsaTbGJEIG8cMfUgJUK&sa=X&oi=book_result&ct=result&resnum=6&ved=0CEAQ6AEwBQ#v=onepage&q=what%20were%20the%20economic%20crimes%20of%20enron&f=false

- Banks defend e-mail about Enron: AS SEEN IN USA TODAY MONEY SECTION, JULY 24, 2002 By Edward Iwata–pdf https://www.usatoday.com/educate/college/business/casestudies/20030128-accountingfraud1.

- Our Fake Energy Crisis, What Really Happened in California, by Harvey Wasserman Copyright 2001, https://www.ratical.org/ratville/dereg/#FEC

- New American: Free Markets, Deregulation and Blame, by Bob Adelmann 19 MARCH 2010

https://www.thenewamerican.com/index.php/history/american/3126-free-markets-deregulation-and-blame - Rose-colored glasses, opaque financial reporting, and investor blues: Enron as con and the vulnerability of Canadian corporate law Publication: St. John’s Law Review By Sarra, Janis - October 1, 2002, https://www.allbusiness.com/business-planning/business-structures-incorporation/1037336-1.html

- Who cleared that Enron exemption? Under Arthur Levitt’s direction – Insight on the News, March 4, 2002 by John Berlau: https://findarticles.com/p/articles/mi_m1571/is_8_18/ai_83699604/

- New technology can help avoid a second Enron: the SEC needs reporting processes for the information ageBy McNamar, R.T.Publication: Regulation September 22 2003– https://www.allbusiness.com/government/advocacy-consumer-protection/684401-1.html

- Senate report blasts SEC’s Enron oversight: by Thor Valdmanis, USA TODAY–https://www.usatoday.com/money/industries/banking/2002-10-06-sec_x.htm

- Is Enron Overpriced? March 5, 2001, by Bethany McLean–Fortune– https://money.cnn.com/2006/01/13/news/companies/enronoriginal_fortune/index.htm

- Who blows the whistle on corporate fraud ? by Alexander Dyek U of Totonto, Adair Morse U of michigan & Luigi Zingales U of Chicago Jan. 2007 –https://escholarship.org/uc/item/07t5k4qj#page-23

Image Credits:

- Farm-Fresh hand at https://commons.wikimedia.org/wiki/File:Farm-Fresh_hand.png

- 30mins220206 by Daryl Campbell at https://commons.wikimedia.org/wiki/File:30mins220206.gif

- Crisis in California by Roger Baxter at https://commons.wikimedia.org/w/index.php?title=File:Crisis_in_California.pdf&page=1

- Citigroup Center, New-York, by Johan Burati at https://commons.wikimedia.org/wiki/File:Citigroup_center.jpg

- JP Morgan Chase Tower in Downtown Houston by WhisperToMe at https://commons.wikimedia.org/wiki/File:EspersonBuildingfromChase.JPG

- CLD at by Nasher52 at https://commons.wikimedia.org/wiki/File:CLD.jpg

- Money market fund by Farcaster at https://commons.wikimedia.org/wiki/File:Money_market_fund.png

- Niszczarka dokumentow.by Julo at https://commons.wikimedia.org/wiki/File:Niszczarka_dokumentow.jpg