The Consequences of Filing for Bankruptcy: What You Need to Know

How Does a Person Become Bankrupt?

Some people may not have any idea about the effects of filing for bankruptcy because the nearest experience they may have is through their participation in a game of “Monopoly”. While it may only be a game, its consequences are near truths as they can depict the circumstances that lead to a declaration of insolvency.

In “Monopoly”, a player becomes insolvent if he or she keeps on investing money in properties without taking into consideration whether there is enough money to pay for other expenses and obligations.

Unless one makes considerable changes, every turn around the board gets the player deeper in debt while paying for the high costs of landing on other players’ properties. Some of the ways to improve one’s finances include investing in houses in order to earn high rental fee, or selling the non-earning properties in order to convert them into cash.

If things get worse, the player may have to resort to mortgaging some or all of the properties owned just to stay alive in the game. However, if there is no improvement in one’s earning capacity, the payment of mortgage debts will only speed up the player’s state of bankruptcy.

Now if a participant has had enough of the game because all he or she does is pay-off creditors and everyone else that person will simply decide to bow out of the game due to insolvency.

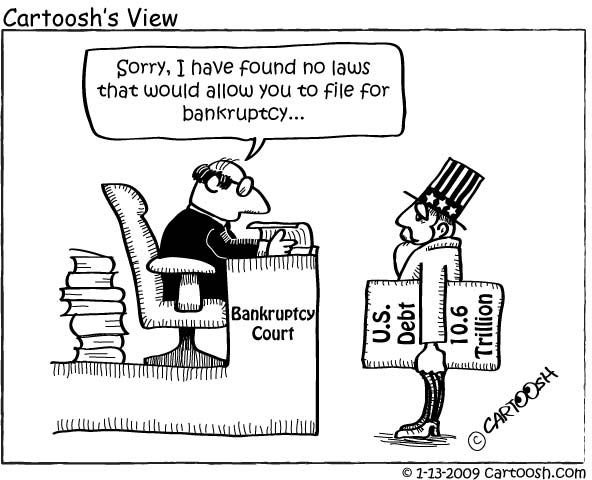

In the real world, you cannot simply bow out of your debts but, in fact, will have to be evaluated to determine if you are eligible for bankruptcy filing.

Adverse Consequences

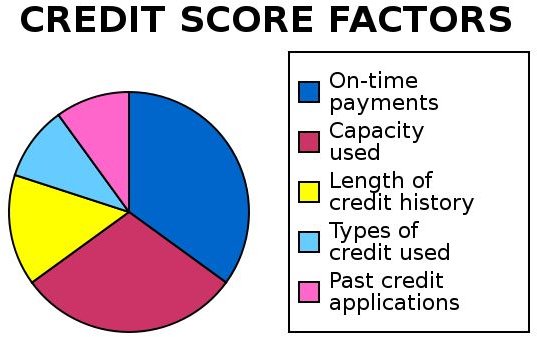

Aside from your social reputation, the one great factor affected is your credit standing. All declarations of insolvency are reported to credit bureaus. These entities store the information in their databases and include it in your credit report for a period of ten years, counting from the date you filed for bankruptcy. In time, you may be able to settle all your debts, but this piece of information will remain in your credit report for about ten years.

During that period, 100 points or more will automatically be deducted to lower your credit score based on the insolvency information. At the same time, there will hardly be any opportunities for you to gain a positive score because lenders such as banks or credit card companies will only turn down your applications.

It is likely that the only score reflected on your credit report is the 100 point-deductible as a result of your bankruptcy declaration. This literally means a negative credit score impact.

What Happens Next

The consequences of filing for bankruptcy in real life are much more complicated. Your social status, your immediate financial obligations, and your future credit eligibility are the things you have to consider. Becoming insolvent is a poor reflection of your buying and paying habits, and lenders will reject any credit applications coming from you.

With the help of a lawyer, all your assets are declared and submitted to a trustee for valuation and will eventually be distributed among your creditors to pay off all the debts you owe. There are several types of bankruptcies to choose from, wherein options on rehabilitation and payment plans will be presented to you, and this includes your future earnings. For the latter, a subsequent “Notice of Garnishment” will be served to your employer by a court appointed sheriff.

Keep it in mind that your eligibility to file for insolvency does not actually relieve you of your credit obligations; it merely relieves you of the pressures of being pressed for payment by your creditors.

Life After Bankruptcy

Whether you like it or not, your life after bankruptcy has been filed becomes stigmatized. That is one of the reasons why you were advised to think things over carefully before deciding to take such action.

At this point, you should increase your efforts in managing your finances in order to avoid another round of financial difficulties. However, it does not mean that credit will no longer be extended to you in case you need it .

There are high-end lenders from whom you can obtain credit despite the insolvency stigma on your record. Again, this is also a matter you should carefully think about since the purpose of the loan may not be worth the credit cost you will be required to pay.

During this period, you are expected to rehabilitate and to improve your credit dealings in order to have a fresh start. You will be encouraged to avail yourself of credit, albeit limited.

This is merely intended to re-develop your sense of responsibility and rebuild another credit history, but this time, you are supposed to aim for a positive one. This is the only way you can show potential lenders you have learned about the consequences of filing for bankruptcy. As a result, you have instilled in yourself a sense of responsibility about handling your credit obligations.

References

- Image of Credit-score-chart by Pne under CC BY SA 2.0

- Image 20090113 bankruptcy-01 by Cartoosh under CC BY SA 3.0

- Image of German Monopoly board by Horst Frank under CC BY SA 3.0

- U.S. Courts.gov— Chapter 11: Reorganization Under the Bankruptcy Code –http://www.uscourts.gov/FederalCourts/Bankruptcy/BankruptcyBasics/Chapter11.aspx